When tax-advantaged accounts come up, 401(k)s and IRAs dominate the conversation. Yet HSAs offer what many financial planners consider the most powerful tax structure in the entire tax code — the only account with a triple tax advantage. For high-income professionals, HSAs are dramatically underutilized. Most treat them as pass-through accounts for current medical bills. Used strategically, they are something else entirely.

The Triple Tax Advantage: A Quick Recap

| Tax Benefit | How It Works |

|---|---|

| Tax-deductible contributions | Money goes in pre-tax, reducing current-year taxable income |

| Tax-free growth | Investments compound without capital gains tax |

| Tax-free withdrawals | Qualified medical expenses withdrawn at any time — years or decades after the contribution — are completely tax-free |

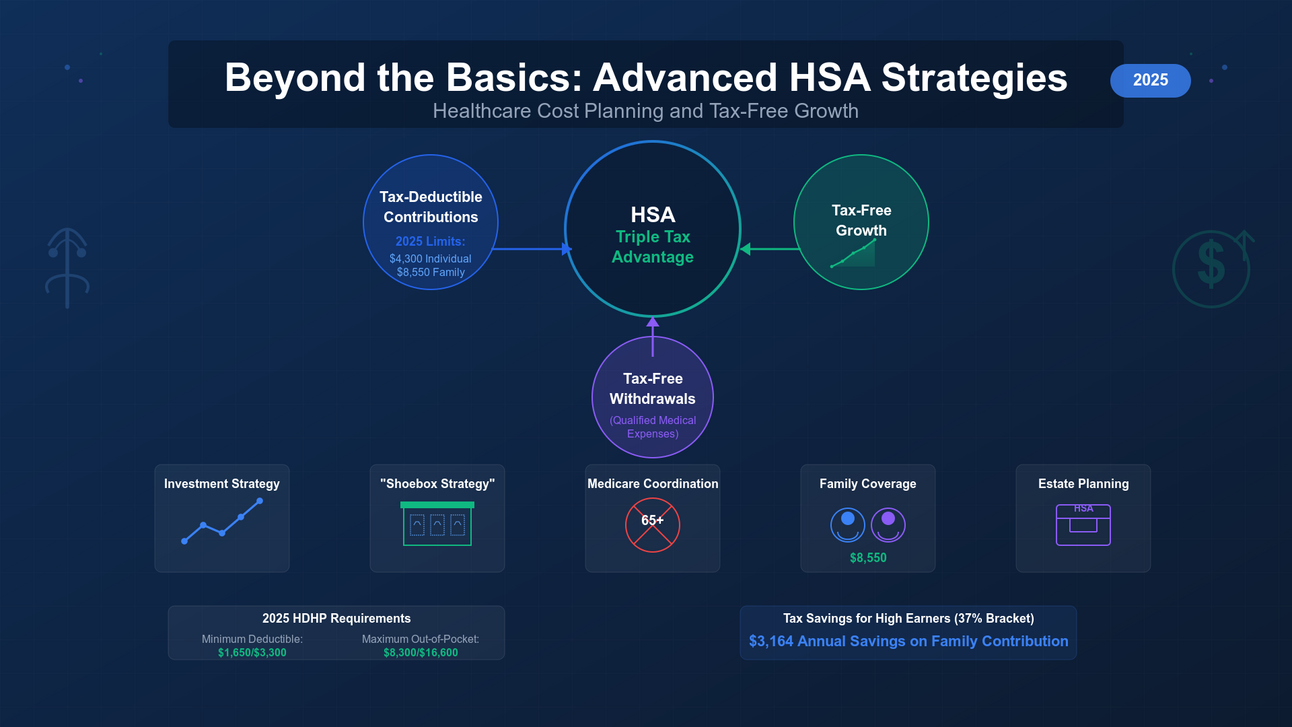

No other account in the tax code offers all 3. A 401(k) gives you 2. A Roth IRA gives you 2 (no deduction on the way in). The HSA gives you all 3, with no income limits for eligibility.

Current HSA Contribution Limits and HDHP Requirements

Contribution limits:

| Coverage Type | Annual Limit | Catch-Up (Age 55+) |

|---|---|---|

| Individual | $4,300 | +$1,000 |

| Family | $8,550 | +$1,000 per eligible spouse |

HDHP minimum requirements to qualify:

| Coverage Type | Minimum Deductible | Maximum Out-of-Pocket |

|---|---|---|

| Individual | $1,650 | $8,300 |

| Family | $3,300 | $16,600 |

Immediate tax savings at the 37% bracket: A high-income professional maximizing the family limit saves $3,164 in federal taxes in the year of contribution — before state income tax savings.

Strategy 1: Transform Your HSA Into an Investment Account

The most common HSA mistake is keeping all funds in cash or a low-yield savings option. Most HSA holders are sitting on an investment account they are treating like a checking account.

How to Reposition

Most HSA providers unlock investment options once the account balance exceeds a threshold — typically $1,000 to $2,000. The quality of investment options varies significantly by provider, which makes provider selection important.

Implementation steps:

- Evaluate your provider’s investment menu. Look for low-expense-ratio index funds (under 0.20%), broad diversification options (domestic, international, bonds), and no additional fees for investing — some providers charge extra for investment access.

- Maintain only a minimal cash reserve. A reasonable target is your expected annual out-of-pocket maximum in cash; invest the rest for long-term growth.

- Consider an HSA rollover if your current options are subpar. Fidelity, Lively, and HSA Authority consistently rank among the top HSA investment providers — all offer low-cost index fund access with no additional investing fees.

- Automate new contributions into investments above your cash threshold so the account doesn’t accumulate uninvested cash by default.

Case Study: Dr. Patricia

Profile: 42-year-old dermatologist, $450,000 income, $24,000 HSA balance sitting entirely in cash at 0.25%.

Action taken:

| Action | Amount |

|---|---|

| Cash reserve retained | $5,000 (roughly annual family out-of-pocket max) |

| Invested in total market index fund | $19,000 |

| Annual new contributions invested above $5,000 threshold | $8,550/year |

Projected outcome by age 65 at 7% annual return:

| Scenario | Projected HSA Value at 65 |

|---|---|

| All cash (0.25% yield) | ~$145,000 |

| Invested strategy | ~$295,000 |

| Difference | ~$150,000 |

All of it is available tax-free for qualified medical expenses. The only variable was where the money was invested.

Strategy 2: The Shoebox Strategy

This is the most powerful underutilized HSA technique available. The IRS does not require you to reimburse yourself for a qualified medical expense in the same year it occurred. You can reimburse yourself for a 2025 medical expense in 2040 — as long as the expense was incurred after you opened your HSA and you have documentation.

How It Works

Pay current medical expenses out-of-pocket. Let the HSA balance grow, invested, for years or decades. Then withdraw HSA funds in retirement by reimbursing yourself for all the documented expenses that accumulated over that time — completely tax-free.

4 requirements the IRS imposes:

- The expense occurred after the HSA was established

- The expense was not reimbursed by insurance

- You did not claim the expense as an itemized deduction

- You have documentation

Documentation System

For each expense, save:

- Itemized receipt (service or product, date, amount)

- Proof of payment

- Insurance Explanation of Benefits (EOB) if applicable

Maintain a running spreadsheet with:

| Column | What to Record |

|---|---|

| Date of service | When the expense occurred |

| Provider | Who provided the service |

| Description | What was treated or purchased |

| Amount | Out-of-pocket cost after insurance |

| Running total | Cumulative unreimbursed balance |

This spreadsheet balance is your “tax-free withdrawal bank” — accessible at any time in retirement by submitting the receipts to your HSA provider.

Case Study: The Martinez Family

Profile: Miguel and Sofia, both 45, tech executives, $600,000 combined income.

Annual strategy:

| Item | Details |

|---|---|

| HSA contribution | $8,550 (family maximum) |

| Annual out-of-pocket medical expenses | $4,200 |

| How expenses are paid | From personal checking — not the HSA |

| HSA funds | Fully invested for long-term growth |

Projected outcome at age 65 (7% annual return):

| Item | Amount |

|---|---|

| HSA balance | ~$400,000 |

| Documented unreimbursed expenses (shoebox) | ~$110,000 |

| Accessible tax-free at any time (by submitting receipts) | ~$110,000 |

| Remaining for future medical expenses | ~$290,000 |

The $110,000 in the shoebox functions like a Roth IRA withdrawal — no income limits, no age restrictions, completely tax-free — because every dollar is backed by a documented medical expense.

Strategy 3: Medicare Coordination — Timing Is Everything

Medicare enrollment ends HSA contribution eligibility. This creates a critical timing decision for high earners who plan to work past 65.

The 3 Medicare Enrollment Scenarios

| Scenario | HSA Contribution Eligibility |

|---|---|

| Receiving Social Security at 65 | Automatic Medicare Part A enrollment — HSA eligibility ends immediately |

| Voluntarily enroll in any part of Medicare | HSA eligibility ends upon enrollment |

| Working with employer coverage, delaying Medicare | Can continue HSA contributions |

The 6-month retroactive enrollment rule: Medicare Part A enrollment is retroactive up to 6 months when you eventually enroll. This means you must stop HSA contributions at least 6 months before Medicare enrollment to avoid a prohibited contribution period.

Advanced Coordination Strategy

For high-income professionals still working past 65 with creditable employer coverage:

- Delay Social Security to at least 65 to avoid automatic Medicare Part A enrollment

- Verify employer coverage qualifies as creditable — your HR department can confirm

- Continue maximizing HSA contributions with the $1,000 catch-up during the delayed years

- Stop HSA contributions 6 months before planned Medicare enrollment

- Enroll in Medicare upon retirement

Case Study: Dr. Williams

Profile: 64-year-old surgeon, $700,000 income, plans to work until 68.

Strategy:

| Age | Action |

|---|---|

| 65 | Verifies employer plan qualifies as creditable coverage; delays Medicare |

| 65 to 67 | Contributes $9,550/year to HSA (family limit + $1,000 catch-up) |

| 67.5 | Stops HSA contributions (6 months before planned retirement) |

| 68 | Retires, enrolls in Medicare |

Result:

| Item | Amount |

|---|---|

| Additional contributions vs. enrolling at 65 | $28,650 (3 years x $9,550) |

| Projected value of those contributions at age 85 (7% return) | ~$115,000 tax-free |

Three years of continued contributions — preserved by a deliberate Medicare enrollment decision — add over $115,000 to Dr. Williams’ tax-free medical spending capacity in retirement.

Strategy 4: Family Coverage Optimization

HSA contribution limits are based on coverage type (individual vs. family) — not marital status. This distinction creates planning opportunities.

Family Coverage Rules That Create Opportunities

| Rule | Planning Opportunity |

|---|---|

| Family coverage limit can be split between spouses’ separate HSAs in any proportion | Diversify investment options; improve estate flexibility |

| Each spouse over 55 must make catch-up contributions to their own HSA | Both spouses need individual HSA accounts to capture both catch-ups |

| Both spouses with separate individual HDHPs get individual limits | May produce higher total contributions than one family plan |

Two-Spouse Comparison: Individual vs. Family HDHP

Case study — The Johnsons: James and Sarah, both 56, executive positions.

| Option | James | Sarah | Total Annual HSA |

|---|---|---|---|

| Both with individual HDHPs | $4,300 + $1,000 catch-up = $5,300 | $4,300 + $1,000 catch-up = $5,300 | $10,600 |

| Family HDHP + two catch-ups | $1,000 catch-up to his HSA | $1,000 catch-up to her HSA | $8,550 + $1,000 + $1,000 = $10,550 |

In their case, maintaining separate individual HDHPs produces $50 more annually in HSA contributions. More importantly, it preserves separate investment accounts, independent beneficiary designations, and flexibility for each spouse to match their own health plan to their individual medical needs.

Key question to evaluate: Does the individual HDHP coverage available from each employer match the health needs of each spouse? If yes, separate plans often win on both benefits and HSA flexibility.

The Catch-Up Rule Most Couples Miss

Each spouse over 55 must make their catch-up contribution to their own HSA — not a shared account. If both spouses are over 55 and only one has an HSA, the family is leaving $1,000 in annual tax-free contributions on the table. Both spouses need individual HSA accounts to capture both catch-ups simultaneously.

Strategy 5: HSA Estate Planning

HSAs are one of the most overlooked components of estate planning. The inheritance treatment varies dramatically based on who inherits — which creates specific planning decisions worth making deliberately.

Inheritance Treatment by Beneficiary Type

| Beneficiary | Tax Treatment at Inheritance |

|---|---|

| Surviving spouse | Converts inherited HSA to their own — all tax advantages preserved |

| Non-spouse individual | HSA loses its status; fair market value becomes taxable income to the beneficiary in the year of death |

| Estate | HSA value becomes taxable income on the decedent’s final return |

| Tax-exempt charity | Passes tax-free — charity pays no income tax |

3 Estate Planning Approaches

Approach 1: Spouse-first beneficiary designation

Name your spouse as primary beneficiary on all HSA accounts. The surviving spouse inherits the HSA without any tax event and can treat it as their own account going forward. This is the default choice for most married couples with substantial HSA balances.

Approach 2: Spend-down strategy for terminal illness

If facing a terminal diagnosis, use HSA funds aggressively for qualified medical expenses before death. Tax-free spending during your lifetime is far more efficient than leaving taxable income to non-spouse heirs. Medical expenses in this period — including home care, specialists, equipment, and medications — are often substantial and fully qualified.

Approach 3: Charitable HSA legacy

Name a tax-exempt organization as beneficiary for a portion of the HSA balance. The charity receives the funds tax-free; the estate avoids the income tax burden that non-spouse heirs would otherwise face. Particularly effective for charitably inclined families with large accumulated HSA balances and non-spouse heirs in high income tax brackets.

Case Study: The Chens

Profile: Robert and Lisa Chen, both 62, $180,000 combined HSA balance built through consistent maximization and investment.

Estate plan:

| Beneficiary | Allocation |

|---|---|

| Spouse (primary) | 100% of each other’s HSA |

| Children (contingent) | 50% of balance |

| Family foundation (contingent) | 50% of balance |

If both Chens pass simultaneously:

- Children receive 50% as taxable income — unavoidable for non-spouse heirs, but the income tax applies only to the fair market value at death, not to growth accumulated over their lifetimes

- Family foundation receives 50% completely tax-free

- Net result: roughly half the accumulated balance passes with no income tax consequence

Your HSA Optimization Roadmap

| Step | Action | Key Details |

|---|---|---|

| 1. Maximize contributions | Verify HDHP qualifies; set up automatic contributions; front-load early in the year | Front-loading maximizes tax-free growth time within the year |

| 2. Reposition into investments | Audit current provider; roll over if options are poor; set cash reserve; automate investing | Keep only the out-of-pocket max in cash; invest the rest |

| 3. Start the shoebox | Build a documentation system today for all future out-of-pocket expenses | Every receipt is a future tax-free withdrawal |

| 4. Plan Medicare timing | If approaching 65 with employer coverage, map out enrollment timeline | Stop contributions 6 months before Medicare enrollment |

| 5. Review estate designations | Update beneficiaries on all HSA accounts; coordinate with overall estate plan | Spouse-first is the baseline; consider charitable designations for excess balances |

The Math: Why the HSA Outperforms

For a high-income professional in the 37% federal bracket making family HSA contributions over 20 years:

| Metric | Amount |

|---|---|

| Annual contribution | $8,550 |

| Annual tax savings (37% federal) | $3,164 |

| Tax savings over 20 years | $63,280 |

| Projected HSA balance at 7% return | ~$450,000 |

| Tax on withdrawal for medical expenses | $0 |

| Equivalent pre-tax value (if taxable) | ~$715,000 |

The HSA produces the equivalent of a $715,000 pre-tax account for someone in the top bracket — because neither the growth nor the withdrawal is ever taxed when used for medical purposes.

This article is for educational and informational purposes only and should not be construed as personalized financial, tax, or legal advice. Tax laws are complex, subject to change, and vary by state and individual circumstance. Contribution limits and HDHP thresholds are adjusted annually by the IRS — verify current figures before making contributions. Consult a qualified tax professional, CPA, enrolled agent, or financial advisor before implementing any strategy discussed here.