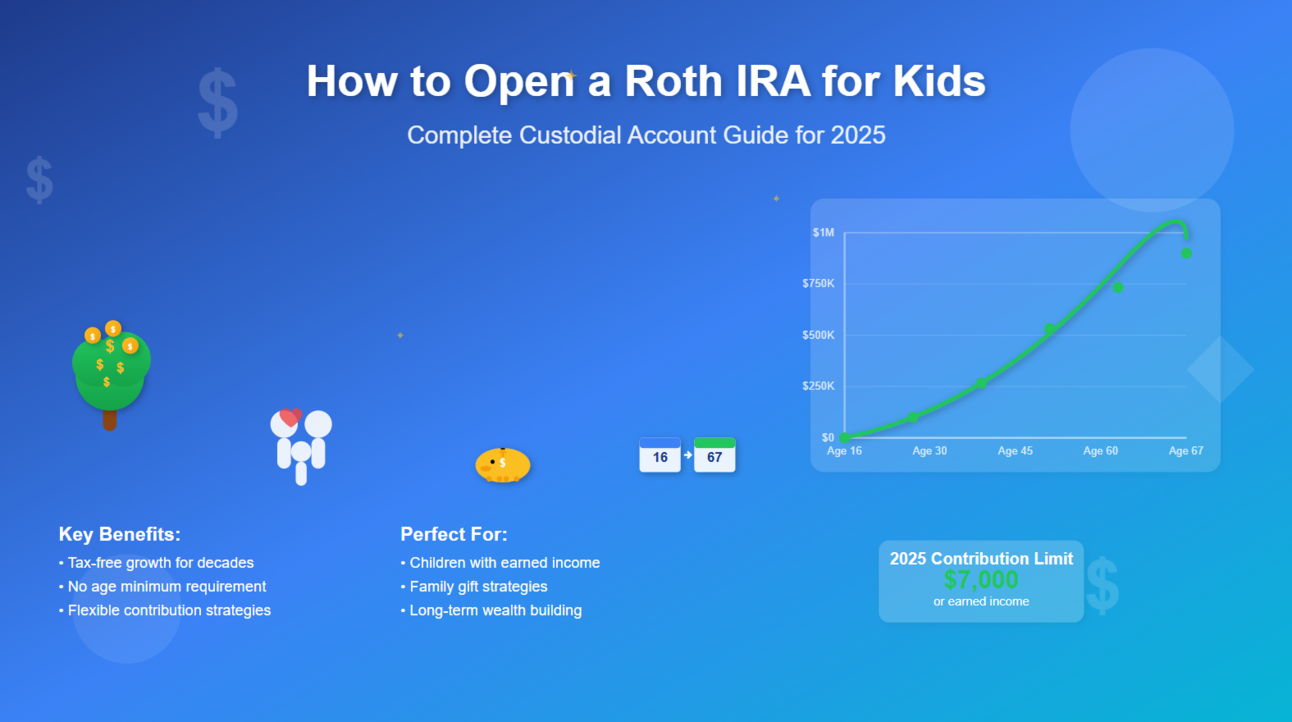

A custodial Roth IRA for a child is one of the most asymmetric financial gifts a parent can give. A single $2,000 contribution made when a child is 16 becomes over $100,000 in tax-free retirement income by age 67 — a 50x return with zero additional input. The mechanics are simple. The obstacles to starting are mostly psychological. This guide covers everything you need to know to set one up, fund it intelligently, and use it strategically.

Why Roth IRAs Are the Right Account for Children

Children and teenagers occupy a unique position in the tax system that makes Roth IRAs exceptionally powerful for them specifically.

The zero-tax starting point: For 2025, children are not required to file a tax return if they earn less than $15,000 (the standard deduction). Most teenage earnings fall entirely within the 0% federal tax bracket. Every dollar contributed to a Roth IRA is contributed post-tax — and for a child paying no income tax, “post-tax” effectively means tax-free forever.

The flexibility advantage: Unlike traditional IRAs, Roth accounts allow contributions (not earnings) to be withdrawn at any time, for any reason, with no taxes or penalties. This makes a Roth IRA a legitimate multi-purpose financial tool — not just a locked-up retirement account.

Useful for major life milestones:

- College expenses

- First-time home purchase (up to $10,000 in earnings withdrawn penalty-free after the 5-year rule is met)

- Starting a business

- Emergency situations

The Rules: Who Can Contribute and How Much

The One Requirement: Earned Income

There is no age minimum for a Roth IRA. A 7-year-old can have one. The only requirement is earned income — and the IRS definition covers far more than a W-2 job.

What counts as earned income for children:

| Category | Examples |

|---|---|

| Traditional employment | Lifeguarding, restaurant work, retail, grocery store |

| Self-employment services | Babysitting, dog walking, lawn mowing, snow shoveling |

| Skills-based work | Tutoring, music lessons, art commissions, photography |

| Technology work | Website design, social media management |

| Sports and recreation | Caddying, coaching youth sports, umpiring games |

2025 Contribution Limits

The 2025 Roth IRA limit is $7,000, but for children the effective cap is the lesser of $7,000 or total earned income for the year.

| Child’s Earned Income | Maximum Roth IRA Contribution |

|---|---|

| $500 (occasional babysitting) | $500 |

| $2,000 (summer job) | $2,000 |

| $5,000 (part-time work) | $5,000 |

| $8,000+ (substantial work) | $7,000 (the annual cap) |

Who Can Make the Contribution

This is frequently misunderstood: anyone can contribute to another person’s Roth IRA, as long as the account owner has the earned income to support it. The money does not have to come from the child’s own paycheck.

This means:

- Parents can fund the full contribution while the child keeps their earnings as spending money

- Grandparents can contribute as a gift

- Multiple family members can contribute toward the same limit

Critical rule: Total contributions from all sources combined cannot exceed the child’s earned income or the $7,000 annual cap, whichever is lower. If the child earned $3,000, the family-wide maximum contribution is $3,000 — not $3,000 each.

The Mathematics of Starting Early

Example 1: The Single Summer Job Contribution

A 16-year-old earns $2,000 working at a local shop. Parents contribute $2,000 to her Roth IRA and let her keep her earnings as spending money. Assumed 7% annual return:

| Age | Account Value |

|---|---|

| 30 | $8,054 |

| 40 | $16,228 |

| 50 | $32,656 |

| 60 | $65,783 |

| 67 (retirement) | $101,677 |

A single $2,000 contribution becomes over $100,000 in tax-free income — a 50x return with no additional contributions.

Example 2: 4 Years vs. 25 Years

| Contributor | Start Age | Years Contributing | Annual Amount | Total Contributed | Value at 67 |

|---|---|---|---|---|---|

| Early starter (son) | 15 | 4 years (ages 15 to 18) | $3,000 | $12,000 | $365,271 |

| Late starter | 25 | 25 years (ages 25 to 50) | $3,000 | $75,000 | $607,529 |

The early starter contributed $63,000 less and still reached 60% of the late starter’s total — from just 4 years of contributions.

Example 3: The Roth IRA Millionaire Path

A child who contributes $3,000 annually from age 16 through age 30 (15 years):

| Metric | Amount |

|---|---|

| Total contributions | $45,000 |

| Value at age 67 (7% return) | $1,284,196 |

$45,000 in contributions — less than many people spend on a car — can produce over $1,000,000 in tax-free retirement wealth.

UGMA vs. UTMA: Which Custodial Structure Applies?

A custodial Roth IRA is held under either the Uniform Gifts to Minors Act (UGMA) or the Uniform Transfers to Minors Act (UTMA). For Roth IRA purposes, both hold standard investment securities — the practical difference is primarily the age at which your child gains full control of the account.

| Feature | UGMA | UTMA |

|---|---|---|

| Created | 1956 (revised 1966) | 1986 |

| Assets allowed | Cash and securities only | Everything in UGMA plus real estate, art, patents, royalties |

| State availability | All 50 states | All states except Vermont and South Carolina |

| Typical transfer age | 18 | 21 (up to 25 in some states) |

For Roth IRA purposes, the asset type distinction is irrelevant — retirement accounts hold cash and securities regardless. The only meaningful variable is when control transfers.

Choosing Your Structure

Choose UGMA if: Your state only offers UGMA (Vermont, South Carolina), or you want the simpler historically-established structure and are comfortable with an age-18 transfer.

Choose UTMA if: You want your child to be older before gaining control, and your state permits age selection (18, 21, or up to 25 depending on state).

The real planning question: An 18-year-old with $15,000+ in a retirement account will make very different decisions than a 25-year-old. If your state allows you to specify a later transfer age, the extra few years of maturity may be worth selecting.

Setting Up a Custodial Roth IRA: Step by Step

What You Need

| Item | Details |

|---|---|

| Child’s full legal name | As it appears on Social Security card |

| Child’s Social Security number | Required for IRS reporting |

| Child’s date of birth | Establishes custodial structure |

| Custodian information | Parent or guardian opening the account |

| Funding source | Bank account for initial transfer |

Choosing a Provider

The major discount brokers — Fidelity, Charles Schwab, and E*TRADE — all offer custodial Roth IRAs. Evaluate on:

- No account minimums or maintenance fees

- Commission-free trading for stocks and ETFs

- Low-cost index fund availability

- Strong online platform and mobile access

- Educational resources for young investors

The Setup Process

- Research providers and compare fees

- Gather required documents (SSNs, addresses, dates of birth)

- Open the custodial account online or by phone (typically under 30 minutes)

- Fund the account via bank transfer

- Choose initial investments

- Set up recurring contributions if planning ongoing deposits

Documentation for Self-Employment Income

If the child does not receive a W-2 (babysitting, lawn mowing, etc.), maintain a log showing:

- Dates of work performed

- Type of work and for whom

- Amount earned

- Any reimbursable expenses

Keep this documentation in case the IRS asks for earned income verification.

Investment Strategy for Young Accounts

With decades until retirement, custodial Roth IRAs can and should be invested aggressively. Young investors can weather market volatility and have every reason to pursue maximum long-term growth.

Recommended Approaches by Age

| Age Range | Recommended Allocation | Notes |

|---|---|---|

| 0 to 25 | 90% to 100% stocks | Maximum growth period; decades to recover from downturns |

| 25 to 35 | 80% to 90% stocks | Gradual shift as career and near-term goals emerge |

| 35+ | Gradual rebalancing | Standard age-appropriate asset allocation |

Best Fund Types for These Accounts

| Fund Type | Why It Works | Typical Expense Ratio |

|---|---|---|

| Total Stock Market Index | Broadest possible US market exposure | Under 0.05% |

| S&P 500 Index | 500 largest US companies, historically strong | Under 0.05% |

| Target-date fund | Automatically rebalances over time; true set-and-forget | 0.10% to 0.20% |

Use the account as an ongoing financial education tool: explain compound interest with real account numbers, discuss market downturns as long-term opportunities, and let teens participate in investment decisions.

Withdrawal Rules: Contributions vs. Earnings

This distinction matters for anyone planning to access the account before retirement.

| Type | Tax Treatment | Penalty | When Available |

|---|---|---|---|

| Contributions | Already taxed — no additional tax | No penalty | Anytime, any reason |

| Earnings | Tax-free if qualified | No penalty if qualified | After age 59½ AND 5-year rule met |

Penalty-Free Early Withdrawal Exceptions for Earnings

Even earnings can be withdrawn without the 10% penalty before age 59½ for:

- First-time home purchase: Up to $10,000 in earnings, penalty-free, after the 5-year rule is satisfied

- Qualified higher education expenses

- Disability

- Medical expenses exceeding 7.5% of AGI

- Health insurance premiums while unemployed

College Planning Consideration

Roth IRA balances are not counted as assets on the FAFSA financial aid application. However, if you withdraw from the account to pay for college, that withdrawal is recorded as income in the year taken and can reduce aid eligibility the following year. Use Roth IRA funds for college as a last resort — after scholarships, grants, and 529 plan funds.

Advanced Strategy 1: Family Business Employment

If you own a business, hiring your minor children creates a triple benefit: work experience, a business tax deduction, and legitimate earned income that qualifies for Roth IRA contributions. This strategy is IRS-approved when executed correctly.

The Tax Math

Scenario: Parent owns a sole proprietorship, pays a 16-year-old $8,000 for legitimate office and social media work.

| Beneficiary | Item | Amount |

|---|---|---|

| Parent | Business expense deduction ($8,000 x 32% bracket) | $2,560 saved |

| Parent | Avoided Social Security/Medicare taxes ($8,000 x 15.3%) | $1,224 saved |

| Parent | Total tax savings | $3,784 |

| Child | Federal income tax owed (under $15,000 standard deduction) | $0 |

| Child | Social Security/Medicare taxes (under 18, parent-owned sole proprietorship) | $0 |

| Child | Available for Roth IRA contribution (2025 limit) | $7,000 |

Business Structures That Qualify for Payroll Tax Exemptions

| Structure | Qualifies? |

|---|---|

| Sole proprietorship owned by parent | Yes |

| Partnership where both partners are parents of the child | Yes |

| Corporation (any type) | No |

| Partnership with non-parent partners | No |

| Estate | No |

For corporations and non-qualifying partnerships, the child’s wages are still a valid business expense — but Social Security and Medicare taxes apply regardless of age.

Age-Appropriate Work by Child’s Age

| Age Range | Appropriate Work |

|---|---|

| 7 to 12 | Filing, light organizing, simple data entry, stuffing envelopes, basic cleaning |

| 13 to 17 | Customer service, social media management, bookkeeping, inventory, marketing assistance |

| Any age | Must be ordinary and necessary for the business; must match the child’s actual capabilities |

What does not qualify: Personal services (babysitting siblings, household chores), work clearly beyond the child’s abilities, or inflated wages not supported by comparable market rates.

IRS Compliance Requirements

- Legitimate work only — ordinary and necessary for the business, actually performed

- Reasonable compensation — compare to what you would pay a non-family employee for the same work

- Proper documentation — timesheets, written job descriptions, W-2 at year-end

Red flags the IRS watches for:

- Wages paid with no corresponding work performed

- Compensation excessive for the work done

- Work inappropriate for the child’s age

- Missing or inconsistent documentation

Getting Started Checklist

- Verify your business structure qualifies for payroll tax exemptions

- Research your state’s child labor laws (hours, work permit requirements, prohibited occupations)

- Identify legitimate, age-appropriate business tasks

- Establish market-rate compensation for the work

- Set up timekeeping and documentation systems

- Consult with a tax professional before implementing

- Open the custodial Roth IRA to receive earned income contributions

Advanced Strategy 2: Multi-Generational Gifting

Because anyone can fund a child’s Roth IRA (up to the child’s earned income), families can coordinate contributions across multiple generations — amplifying the retirement savings benefit without triggering gift tax consequences.

Gift Tax Basics for 2025

| Rule | Amount |

|---|---|

| Annual gift tax exclusion per recipient, per giver | $19,000 |

| Married couple combined (gift-splitting) | $38,000 per recipient |

| Lifetime exemption | $13.99 million |

| Roth IRA maximum contribution | $7,000 |

The $7,000 Roth IRA contribution limit is well under the $19,000 annual exclusion. No gift tax return is required for Roth IRA contributions within the annual exclusion.

Coordination Rules

The absolute contribution limit is the child’s earned income or $7,000 — whichever is lower — across all contributors combined. If 4 grandparents, 2 parents, and 3 aunts all want to contribute to a child who earned $3,000, the total from everyone together is still capped at $3,000.

Family Contribution Scenarios

Scenario — 16-year-old Sarah earns $5,000:

| Contributor | Contribution |

|---|---|

| Parents | $3,000 |

| Grandparents | $2,000 |

| Total | $5,000 (equal to earned income — correct) |

| Gift tax impact | $0 — well under each contributor’s $19,000 exclusion |

Matching strategies (all assume child earned $5,000):

| Approach | Child Contributes | Family Contributes | Total |

|---|---|---|---|

| Dollar-for-dollar match | $2,500 | $2,500 | $5,000 |

| Enhanced family match | $1,000 | $4,000 | $5,000 |

| Full family funding | $0 (keeps all earnings) | $5,000 | $5,000 |

Multi-Child Family Example

Family with 3 working children:

| Child | Earned Income | Family Contribution | Roth IRA Funded |

|---|---|---|---|

| Child A (age 14) | $3,000 | $3,000 | $3,000 |

| Child B (age 16) | $5,000 | $5,000 | $5,000 |

| Child C (age 17) | $7,000+ | $7,000 | $7,000 |

| Total | $15,000 | $15,000 |

Parents’ combined annual exclusion: $38,000. Total gifted: $15,000. No gift tax filing required.

The Johnson Family — Long-Term Compound Effect

| Year | Jake’s Age | Earned Income | Family Contribution | Cumulative Contributions |

|---|---|---|---|---|

| Year 1 | 14 | $2,000 | $2,000 | $2,000 |

| Year 2 | 15 | $3,000 | $3,000 | $5,000 |

| Year 3 | 16 | $4,000 | $4,000 | $9,000 |

| Year 4 | 17 | $5,000 | $5,000 | $14,000 |

Estimated value at Jake’s age 67 (7% return): $424,000 — from $14,000 in total contributions, all within gift tax exclusion limits.

Gift Tax Reporting Note

Contributions within the annual exclusion require no IRS reporting. If contributions ever exceed the $19,000 per-giver threshold, Form 709 (Gift Tax Return) must be filed — but no gift tax is owed until cumulative lifetime gifts exceed the $13.99 million exemption.

State-by-State Custodial Transfer Ages

The age at which your child gains full control of the account depends on your state and account type.

States with UTMA Transfer at Age 18

Arkansas, California, District of Columbia, Kentucky, Louisiana, Maine, Maryland, Michigan, Nevada, Oklahoma, South Dakota, Virgin Islands

States with UTMA Transfer at Age 21

Alabama, Alaska, Arizona, Colorado, Connecticut, Delaware, Florida, Georgia, Hawaii, Idaho, Illinois, Indiana, Iowa, Kansas, Massachusetts, Minnesota, Mississippi, Missouri, Montana, Nebraska, New Hampshire, New Jersey, New Mexico, New York, North Carolina, North Dakota, Ohio, Oregon, Pennsylvania, Rhode Island, Tennessee, Texas, Utah, Vermont, Virginia, Washington, West Virginia, Wisconsin, Wyoming

States with Flexible Age Ranges

| State | Standard Age | Maximum Allowed |

|---|---|---|

| Alaska | 21 | 25 (custodian can specify) |

| California | 18 | 21 for gifts; 25 for will/trust transfers |

| Florida | 21 | 25 (with required notice at age 21) |

| Nevada | 18 | 25 |

| New Jersey | 18 | 21 (custodian can specify) |

| North Carolina | 18 | 21 (custodian can specify) |

| Ohio | 21 | 25 |

| Oregon | 21 | 25 (custodian can specify) |

| Pennsylvania | 21 | 25 (custodian can specify) |

| Tennessee | 21 | 25 (custodian can specify) |

| Virginia | 21 | 25 |

| Washington | 21 | 25 |

| Wyoming | 21 | 30 (must notify minor at age 21) |

States with Limitations

| State | Situation |

|---|---|

| South Carolina | UTMA not available — UGMA only, transfers at age 18 |

| Vermont | Limited UTMA availability — primarily UGMA accounts |

Planning note: In states that allow you to specify a transfer age, consider the maturity level you expect your child to have at different ages. The choice is often permanent once the account is established. A child gaining control of a $15,000+ account at 18 faces very different pressures than one gaining control at 25.

Your Action Plan: 6 Steps to Get Started

| Step | Action | Notes |

|---|---|---|

| 1 | Identify earning opportunities | Age-appropriate jobs, family business work, or self-employment services |

| 2 | Research and choose a provider | Compare fees, investment options, and platform quality |

| 3 | Open the account | Gather SSNs, dates of birth, and addresses; most accounts open in under 30 minutes |

| 4 | Decide your contribution strategy | Child funds their own; parents match; family fully funds; some combination |

| 5 | Choose initial investments | Start simple — a total market index fund or target-date fund |

| 6 | Monitor and educate | Review annually with the child; use real account numbers to teach compound interest |

Common Questions

“My child is too young to worry about retirement.”

This misses the point. The younger the start, the less the child will need to save later. 4 years of contributions between ages 15 and 18 can produce the same retirement wealth as 25 years of contributions starting at age 25 — with $63,000 less contributed.

“What if my child spends it all when they turn 18?”

When the account transfers, the child can withdraw contributions anytime or liquidate the account entirely. Mitigating factors: the financial education built through managing the account, the fact that contributions are already accessible (so restricted access isn’t the protection), and that many young adults understand the value of a growing account better than expected. Prepare them with financial education well before the transfer age.

“Self-employment income for kids seems complicated.”

It is not. The child’s self-employment income may need to be declared as taxable, but most children will owe nothing after applying the standard deduction. The paperwork is a Schedule C and basic income records. Most cases take under an hour to document.

“What about self-employment tax?”

Children earning over $400 in net self-employment income may owe self-employment tax (15.3%) on those earnings. This also means they are earning Social Security credits — a long-term benefit. For children employed in a parent-owned sole proprietorship, those wages are exempt from Social Security and Medicare taxes until age 18.

The Bottom Line

Setting up a custodial Roth IRA for a child is one of the highest-ROI financial moves available. The math is unambiguous: starting early with modest amounts consistently outperforms starting late with large amounts. Your teenager’s summer job earnings — even just $1,000 to $2,000 — can become $50,000 to $100,000 in tax-free retirement income with zero additional contributions.

The best time to start was when your child first earned money. The second-best time is today.

This article is for educational and informational purposes only and should not be construed as personalized financial, tax, or legal advice. Tax laws are complex, subject to change, and vary by state and individual circumstance. Strategies discussed are based on 2025 tax law and may become outdated as legislation evolves. Before implementing any strategy discussed here, consult a qualified tax professional, CPA, enrolled agent, or financial advisor who can evaluate your specific situation. Investment strategies carry inherent risk; past performance does not guarantee future results.