High-income professionals hit the same wall quickly in retirement planning. Direct Roth IRA contributions phase out at certain income thresholds. Standard 401(k) employee deferrals are capped at $23,500. For someone earning $300,000, $450,000, or more, these limits leave an enormous gap between what they can save tax-efficiently and what they actually need to save.

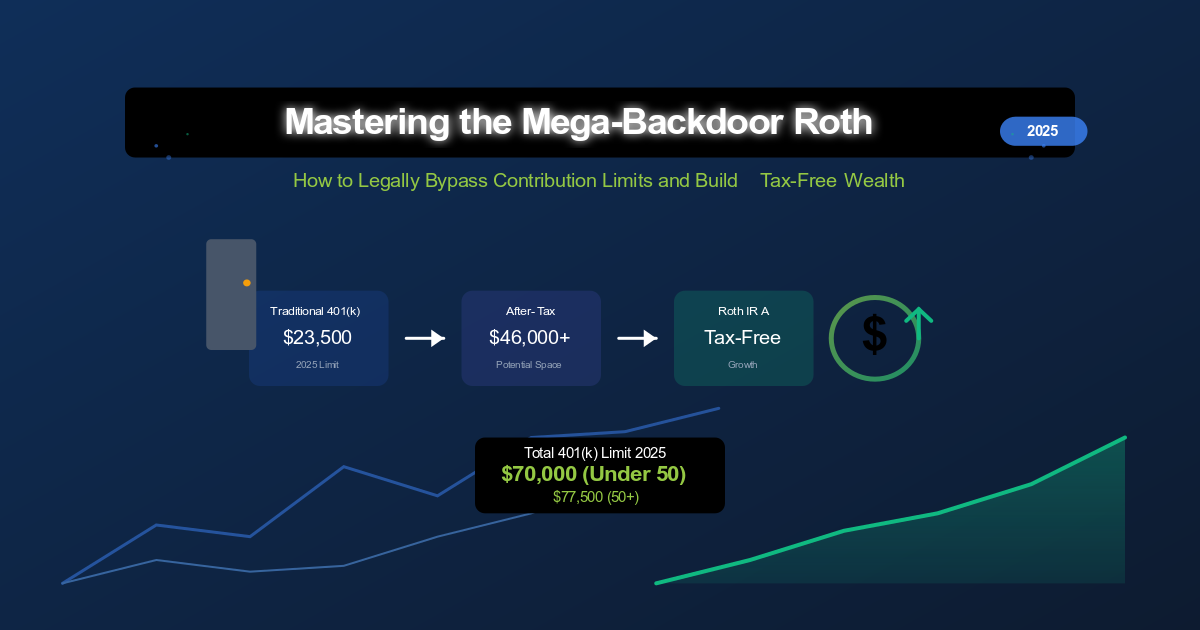

The Mega-Backdoor Roth closes part of that gap. Done correctly, it can add up to $46,000+ annually to a Roth account — completely legally, using a provision that has survived multiple rounds of tax legislation. The catch: your employer’s 401(k) plan must allow it, and most people have never thought to check.

The Contribution Limit Problem

The total 401(k) contribution limit — combining employee deferrals, employer contributions, and after-tax contributions — is $70,000 for those under 50, or $77,500 for those 50 and older. Most people only use the employee deferral slice.

2025 contribution limits at a glance:

| Contribution Type | Under 50 | Age 50+ |

|---|---|---|

| Employee deferrals (pre-tax or Roth) | $23,500 | $31,000 |

| Employer contributions (match/profit-sharing) | Varies | Varies |

| After-tax non-Roth contributions | Up to remaining space | Up to remaining space |

| Total 401(k) limit (all sources combined) | $70,000 | $77,500 |

| Standard Backdoor Roth IRA | $7,000 | $8,000 |

The available space calculation:

After-tax contribution capacity = $70,000 − (employee deferrals + employer contributions)Example: You contribute $23,500 and receive $10,000 in employer matching. Your remaining after-tax contribution capacity is $36,500.

How the Mega-Backdoor Roth Works: 3 Steps

Step 1: Make After-Tax (Non-Roth) Contributions

After-tax non-Roth contributions are a third type of 401(k) contribution — distinct from pre-tax deferrals and from designated Roth contributions. They go in with after-tax dollars, but the earnings grow tax-deferred and would be taxed as ordinary income on withdrawal. On their own, they are not especially efficient.

The efficiency comes from what you do next.

Step 2: Convert or Roll Over to Roth — Immediately

Converting after-tax contributions to Roth status — either within the plan (in-plan Roth conversion) or by rolling them out to a Roth IRA (in-service withdrawal) — transforms ordinary tax-deferred dollars into tax-free Roth assets.

The key word is immediately. If earnings accumulate before conversion, those earnings become taxable at conversion. Make the contribution, then convert within days — ideally within the same pay period if automatic conversions are available.

Step 3: Track and Report Correctly

After-tax contributions generate a Form 1099-R when converted or rolled over. If handled promptly, the taxable amount is minimal or zero. File correctly to establish the basis and avoid the IRS treating the full amount as taxable.

The 2 Plan Features You Must Have

This strategy only works if your employer’s 401(k) plan offers both of these:

| Required Feature | What It Is | Why It Matters |

|---|---|---|

| After-tax (non-Roth) contributions | Ability to contribute beyond the employee deferral limit with after-tax dollars | Without this, the strategy cannot start |

| In-plan Roth conversion OR in-service withdrawals | Either the ability to convert after-tax funds to Roth within the plan, or to roll them out to a Roth IRA while still employed | Without one of these, after-tax contributions sit as inefficient tax-deferred savings until you leave the employer |

Approximately 43% of employer 401(k) plans offer after-tax contributions — more common among large employers and in industries with highly compensated workforces. The features are less visible than basic plan options; many participants never know they exist.

How to Check If Your Plan Qualifies

Option 1 — Read the Summary Plan Description (SPD). Every plan participant is entitled to a copy. Search for: “after-tax contributions,” “in-service withdrawals,” “in-plan Roth conversions,” or “Roth in-plan rollovers.”

Option 2 — Ask your benefits or HR department. Request a meeting or email with these specific questions:

- “Does our 401(k) plan allow after-tax contributions beyond the employee deferral limit?”

- “If yes, what is the maximum percentage of compensation allowed?”

- “Does our plan allow in-service withdrawals of after-tax contributions?”

- “Does our plan allow in-plan Roth conversions of after-tax contributions?”

Get the answers in writing. HR staff sometimes confuse “Roth 401(k) contributions” (designated Roth) with “after-tax non-Roth contributions” — they are different features.

Step-by-Step Implementation

If Your Plan Offers In-Plan Roth Conversions

| Step | Action | Notes |

|---|---|---|

| 1 | Set up after-tax contributions via payroll | Specify “after-tax non-Roth” — not Roth 401(k) |

| 2 | Set up automatic in-plan conversions if available | Eliminates earnings accumulation problem entirely |

| 3 | If automatic not available, convert manually on a regular schedule | Weekly or bi-weekly; do not let earnings accumulate |

| 4 | Verify Form 1099-R is issued for the conversion | Taxable amount should be minimal if converted promptly |

| 5 | File Form 8606 if rolling to a Roth IRA | Establishes basis for proper tax treatment |

If Your Plan Offers In-Service Withdrawals Only

| Step | Action | Notes |

|---|---|---|

| 1 | Open a Roth IRA if you don’t already have one | Any major custodian works |

| 2 | Set up after-tax contributions via payroll | Specify “after-tax non-Roth” |

| 3 | Submit rollover paperwork on a regular schedule | Quarterly is common; more frequent is better |

| 4 | Request a direct rollover — check payable to “Roth IRA custodian FBO [your name]“ | Direct rollover avoids 20% mandatory withholding |

| 5 | Deposit into Roth IRA within 60 days | Direct rollovers preferred over 60-day indirect rollovers |

| 6 | Track transactions for tax reporting | Maintain contribution records separately from other IRA basis |

3 Real-World Examples

Example 1: Dr. Chen — Maximum Strategy, In-Plan Conversion

Profile:

| Item | Detail |

|---|---|

| Age | 45 |

| Annual income | $450,000 |

| Plan features | After-tax contributions + in-plan Roth conversions available |

2025 contribution breakdown:

| Source | Amount | Account Type |

|---|---|---|

| Employee deferrals | $23,500 | Traditional 401(k) |

| Employer match (5%) | $22,500 | Traditional 401(k) |

| After-tax contributions | $24,000 | Converted to Roth 401(k) |

| Total | $70,000 |

Dr. Chen sets up automatic bi-weekly in-plan Roth conversions to minimize taxable earnings. By year-end, she has added $24,000 to her Roth account that would have been impossible through direct Roth IRA contributions at her income level.

20-year projection on a single year’s $24,000 Roth contribution at 7% annual return: ~$93,000 tax-free.

Example 2: James — Partial Strategy, In-Service Withdrawals

Profile:

| Item | Detail |

|---|---|

| Age | 38 |

| Annual income | $240,000 |

| Plan features | After-tax contributions + in-service withdrawals (no in-plan conversion) |

2025 contribution breakdown:

| Source | Amount | Account Type |

|---|---|---|

| Employee deferrals (Roth) | $23,500 | Roth 401(k) |

| Employer match | $12,000 | Traditional 401(k) |

| After-tax contributions (partial) | $18,000 | Rolled to Roth IRA quarterly |

| Total | $53,500 |

James has $34,500 in theoretical after-tax capacity but uses $18,000 due to other financial priorities. He submits quarterly rollover paperwork, requesting direct rollovers to his Roth IRA. He adds $18,000 to his Roth IRA that was categorically unavailable via direct contribution at his income level.

Result: Not a maximal execution, but a meaningful and repeatable Roth addition each year — with room to scale up as cash flow allows.

Example 3: Maria — Self-Employed, Solo 401(k)

Profile:

| Item | Detail |

|---|---|

| Age | 52 |

| Annual income | $300,000 (single-member LLC) |

| Plan | Solo 401(k) designed to allow after-tax contributions and in-plan Roth conversions |

2025 contribution breakdown:

| Source | Amount | Account Type |

|---|---|---|

| Employee deferrals (incl. $7,500 catch-up) | $31,000 | Traditional Solo 401(k) |

| Employer profit-sharing contribution | $30,000 | Traditional Solo 401(k) |

| After-tax contributions | $16,500 | Immediately converted to Roth |

| Total | $77,500 | (age 50+ limit) |

Maria establishes her Solo 401(k) specifically to include after-tax contribution and in-plan Roth conversion features — not all Solo 401(k) plan documents include these. She converts after-tax contributions immediately upon contribution to minimize taxable earnings.

Key point for self-employed: Solo 401(k) plan documents must explicitly permit after-tax contributions and in-plan Roth conversions. Off-the-shelf Solo 401(k) templates often omit these features. Work with a plan document specialist to ensure the features are properly drafted.

5 Common Pitfalls

Pitfall 1: Confusing this with the regular Backdoor Roth IRA

The pro-rata rule — which creates tax complications when converting traditional IRA funds to Roth — does not apply to the Mega-Backdoor Roth. You are dealing with after-tax 401(k) contributions, not IRA funds. These are separate strategies with separate tax mechanics. Keep documentation for each strategy completely distinct.

Pitfall 2: Letting earnings accumulate before conversion

If after-tax contributions sit invested for months before conversion, the earnings become taxable at conversion. The fix: convert as immediately as possible after each contribution. Automatic in-plan conversions eliminate this problem entirely.

Pitfall 3: Triggering plan non-discrimination testing failures

401(k) plans must pass annual non-discrimination testing. If highly compensated employees make heavy after-tax contributions while non-highly compensated employees do not, the plan may fail testing. Discuss your intentions with the plan administrator before starting. Spreading contributions throughout the year is preferable to large lump-sum contributions.

Pitfall 4: Mishandling the rollover mechanics

When rolling to a Roth IRA via in-service withdrawal, always request a direct rollover — check made payable to the Roth IRA custodian “FBO [your name].” A check made payable to you triggers mandatory 20% withholding, which you would then need to make up out-of-pocket to complete the full rollover within 60 days.

Pitfall 5: Rolling pre-tax money to a Roth IRA by mistake

Only after-tax contributions (and their earnings) receive the specialized Mega-Backdoor Roth treatment. Pre-tax employee deferrals, employer contributions, and their earnings must roll to a traditional IRA or remain in the 401(k). When submitting rollover paperwork, explicitly specify “after-tax non-Roth contributions only.”

Legislative Risk: How Durable Is This Strategy?

Several tax reform proposals have targeted backdoor Roth strategies. The concern is legitimate. The honest assessment:

| Factor | Impact on Risk |

|---|---|

| Legislative history | The strategy has survived multiple reform cycles since gaining popularity |

| SECURE and SECURE 2.0 Acts | Both focused on expanding retirement savings options, not restricting them |

| Retroactivity | Tax changes to retirement accounts typically include grandfathering provisions — money already in Roth status would likely remain protected |

| Prospective changes | Future legislation could eliminate the strategy for new contributions; already-converted funds would likely be unaffected |

Practical response: Take advantage of the strategy while it exists. Diversify across account types (traditional, Roth, and taxable) rather than concentrating entirely in one structure. Stay current on proposed legislation. Converted Roth funds are the most durable — the risk is primarily to future contribution capacity, not past conversions.

How the Mega-Backdoor Roth Fits With Other Strategies

| Strategy | Relationship |

|---|---|

| Regular Backdoor Roth IRA | These run simultaneously — add $7,000 (or $8,000 if 50+) to Roth IRA on top of Mega-Backdoor Roth contributions |

| HSA | Maximize before implementing Mega-Backdoor Roth — HSA offers triple tax advantage with lower contribution limits ($4,300 individual / $8,550 family) |

| Traditional 401(k) vs. Roth balance | Mega-Backdoor Roth builds the Roth side; maintain some pre-tax savings for tax bracket flexibility in retirement |

| Tax bracket management | Strategy is most compelling when you expect retirement tax rates to be similar to or higher than current rates |

Is This Strategy Right for You?

| Situation | Fit |

|---|---|

| Already maximizing regular 401(k) deferrals | Strong fit — this is the natural next step |

| HSA and Backdoor Roth IRA already maxed | Strong fit |

| Employer plan allows both required features | Required — confirm before proceeding |

| Additional cash flow available beyond standard savings | Required — after-tax contributions come from take-home pay |

| Expecting similar or higher tax bracket in retirement | Strong fit |

| Not yet maxing out regular 401(k) | Address that first |

| High-interest debt outstanding | Pay that down before adding complexity |

| Plan does not allow required features | Strategy is unavailable — consider other options (HSA, Backdoor Roth IRA, taxable account) |

| Expecting significantly lower tax bracket in retirement | Traditional pre-tax contributions may produce better outcome |

The Long-Term Math

An additional $30,000 per year contributed to a Roth account over 20 years at a 7% annual return produces approximately $1.3 million in completely tax-free retirement assets. For a high-income professional in the 37% bracket in retirement, the tax value of that Roth balance — compared to an equivalent traditional account requiring ordinary income tax on every withdrawal — represents hundreds of thousands of dollars in lifetime tax savings.

The strategy is not automatic and requires annual effort to implement correctly. But for those whose employer plans support it, the Mega-Backdoor Roth is one of the most powerful tax-free wealth-building tools available in the current tax code.

This article is for educational and informational purposes only and should not be construed as personalized tax, financial, or legal advice. Contribution limits, income thresholds, and plan rules are subject to change by Congress or the IRS. Individual plan features vary significantly — verify your specific plan’s provisions with your plan administrator and plan documents before implementing any strategy described here. Consult a qualified tax professional, CPA, enrolled agent, or financial advisor before implementing this or any other retirement planning strategy.