Imagine spending 30 years building a comfortable retirement nest egg, paying off your mortgage, and carefully investing in your 401(k). You’ve done everything right financially. Yet when you pass away, your family discovers that a significant portion of your life’s work could disappear to taxes before they see a penny.

Major federal tax law changes in 2025 dramatically reduced this threat for most American families — but estate taxes remain a critical concern that extends far beyond the ultra-wealthy. The key shift: for most middle-class families, the estate tax challenge has moved from federal concerns to state-level taxes that can still claim substantial portions of family wealth.

Understanding Estate Tax Fundamentals

Estate Tax vs. Inheritance Tax: The Key Distinction

| Tax Type | Who Pays | Who Imposes It |

|---|---|---|

| Estate tax | The estate itself, before assets are distributed | Federal government + 12 states |

| Inheritance tax | The individuals who receive the assets | 6 states (some have both) |

Estate tax is essentially the government’s final claim on your accumulated wealth — a “privilege tax” for passing wealth to the next generation.

The Federal Estate Tax Framework

The federal estate tax adds up everything you own at death. If the total exceeds the unified credit exemption, the excess gets taxed at rates up to 40%.

Key federal exemption milestones:

| Period | Per Person | Married Couple (Combined) |

|---|---|---|

| 2025 (pre-OBBBA) | $13.99 million | $27.98 million |

| 2026+ (OBBBA permanent) | $15 million | $30 million |

The OBBBA increase is permanent and indexed for inflation — eliminating federal estate tax concerns for the vast majority of American families. This fundamentally shifts estate tax planning toward state-level considerations.

Why State Estate Taxes Now Take Center Stage

The OBBBA removed federal estate taxes from most families’ planning equations — but left state estate tax systems completely unchanged. Federal and state tracks now move in opposite directions, creating new planning opportunities and challenges that didn’t exist before.

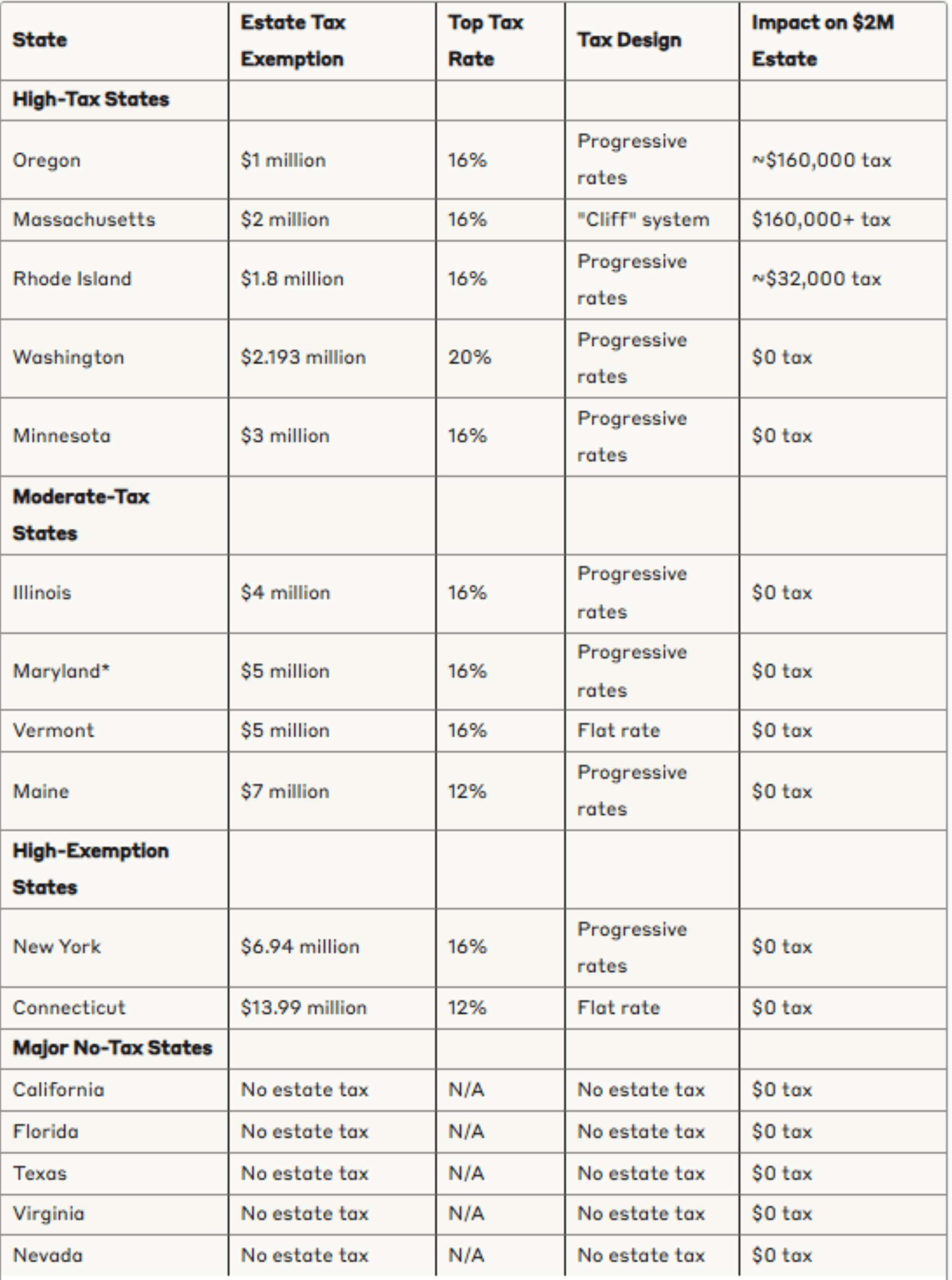

State-by-State Estate Tax Comparison

Maryland also imposes a 10% inheritance tax on certain beneficiaries.

Key patterns from this table:

- Exemptions range from Oregon’s $1 million to Connecticut’s $13.99 million

- 33 states (including California, Texas, and Florida) impose no estate or inheritance taxes at all

- Identical families in different states can face tax bills ranging from $0 to $320,000+

The Massachusetts “Cliff” Problem

Massachusetts uses a “cliff” system that creates one of the most extreme tax design consequences in the country.

How most states work (progressive): Only the amount above the exemption gets taxed.

How Massachusetts works (cliff): If your estate exceeds $2 million, the entire estate — not just the excess — is taxable.

| Estate Value | Massachusetts Tax |

|---|---|

| $1,999,999 | $0 |

| $2,000,001 | ~$160,000+ |

Adding $20,000 to your estate can trigger a $160,000 tax bill. This creates a genuine planning imperative that doesn’t exist in progressive systems: families may actually benefit from deliberately reducing their estate below the cliff threshold.

Real-World Impact: How the OBBBA Affects Families Today

Scenario 1: The Oregon Family

The Johnson Family — retired teachers, Oregon residents:

| Asset | Value |

|---|---|

| Home (purchased for $180,000 in 1995) | $650,000 |

| Combined retirement accounts | $580,000 |

| Life insurance | $200,000 |

| Other investments | $170,000 |

| Total estate | $1,600,000 |

Tax analysis under current law:

| Tax Level | Calculation | Amount Owed |

|---|---|---|

| Federal | $1.6M far below $30M combined exemption | $0 |

| Oregon state | $1,600,000 - $1,000,000 exemption = $600,000 taxable | ~$60,000 |

| Total estate tax | $60,000 |

Before OBBBA, this family faced potential exposure to both federal and state taxes. Now their entire tax burden is a state tax issue — making the planning strategy clearer and more targeted.

Scenario 2: The Seattle Technology Family

Combined estate: $4.2 million

| Asset | Value |

|---|---|

| Primary residence (Seattle) | $1,800,000 |

| Retirement accounts | $1,200,000 |

| Stock options and investments | $900,000 |

| Business interests | $300,000 |

| Total | $4,200,000 |

Tax analysis:

| Tax Level | Calculation | Amount Owed |

|---|---|---|

| Federal | $4.2M below $30M combined exemption | $0 |

| Washington state | $4,200,000 - $2,193,000 = $2,007,000 taxable at progressive rates | ~$285,000 |

This family’s $1.8M home may have been purchased for $400,000 20 years ago. Real estate appreciation in high-cost markets routinely pushes middle-class families into state estate tax territory — without their lifestyle ever feeling “wealthy.”

The Geographic Arbitrage Reality: Same $3M Family, Different States

| State | Estate Tax Owed | Why |

|---|---|---|

| Oregon | ~$320,000 | Low $1M exemption, progressive rates |

| Massachusetts | ~$320,000+ | Cliff effect on full estate |

| Washington | ~$145,000 | Moderate exemption, progressive rates |

| New York | $0 | High exemption protects this estate |

| Connecticut | $0 | Even higher exemption |

| Florida / Texas / Nevada | $0 | No state estate tax |

The range from $0 to $320,000+ results entirely from state tax policy — not from any difference in the family’s wealth or behavior.

Strategic Solutions for the Post-OBBBA Environment

Estate tax planning has 3 core approaches: avoid the tax through geographic planning, reduce the tax through wealth transfer, or plan for the tax through liquidity management.

Strategy 1: Geographic Optimization

Moving to a no-tax state has become the most straightforward and often most valuable estate tax strategy since the OBBBA removed federal considerations for most families.

The 33 states with no estate or inheritance taxes:

Alabama, Alaska, Arizona, Arkansas, California, Colorado, Delaware, Florida, Georgia, Idaho, Indiana, Kansas, Louisiana, Michigan, Mississippi, Missouri, Montana, Nevada, New Hampshire, New Mexico, North Carolina, North Dakota, Ohio, Oklahoma, South Carolina, South Dakota, Tennessee, Texas, Utah, Virginia, West Virginia, Wisconsin, and Wyoming.

The 183-Day Rule — how domicile is established:

Spending 183 or more days per year in a state generally establishes tax residency. But high-tax states have become aggressive in challenging former residents — especially when substantial estate tax savings are involved. Day-counting is just the beginning.

What tax authorities actually examine:

| Evidence Category | Examples |

|---|---|

| Documentation | Voter registration, driver’s license, professional licenses |

| Financial connections | Bank accounts, investment accounts, insurance policies |

| Medical and social ties | Primary care physician, club memberships, religious affiliation |

| Physical presence | Travel logs, credit card receipts, utility bills |

| Property | Whether homestead exemption is claimed in former state |

3-step domicile establishment process:

Step 1: Document your new residency pattern

- Keep a detailed daily travel log

- Save credit card statements and receipts confirming your location

- Maintain phone records and utility bills

Step 2: Change everything systematically

- Driver’s license, voter registration, bank and investment accounts

- Insurance policies (auto, homeowners, health)

- Will and estate planning documents reflecting new domicile

- Partial changes undermine your residency claim

Step 3: Sever old ties completely

- Remove homestead exemptions from former state property

- Transfer professional licenses and memberships

- Update all mailing addresses, subscriptions, and affiliations

- The goal: no evidence that your primary life connections remain in the former high-tax state

Strategy 2: Systematic Wealth Transfer Through Gifting

Assets you no longer own cannot be taxed in your estate. Gifting reduces estate value while allowing you to see beneficiaries benefit during your lifetime.

Annual exclusion gifting (2024 amounts):

| Giver | Per Recipient Per Year | No gift tax return required? |

|---|---|---|

| Individual | $18,000 | Yes |

| Married couple (combined) | $36,000 | Yes |

Important: gift recipients owe no income tax on money received. Gifts are not taxable income to the recipient. Gifts within annual exclusion limits also don’t reduce your $15 million lifetime federal exemption — they’re completely separate.

The Johnson family example — eliminating Oregon estate tax through gifting:

The Johnsons face ~$60,000 in Oregon estate tax on their $1.6M estate. With 2 children and 4 grandchildren (6 recipients):

| Year | Annual Gifts (6 recipients x $36,000) | Cumulative Reduction |

|---|---|---|

| Year 1 | $216,000 | $216,000 |

| Year 2 | $216,000 | $432,000 |

| Year 3 | $216,000 | $648,000 |

| Year 4 | $216,000 | $864,000 |

| Year 5 | $216,000 | $1,080,000 |

After 5 years, $1,080,000 has been removed from the estate — likely eliminating their Oregon exposure entirely. No gift tax returns required. No impact on lifetime exemptions.

529 Plan front-loading:

529 education savings plans allow “superfunding” — contributing up to 5 years of annual exclusions in a single year:

| Giver | Single-Year Superfund Amount Per Beneficiary |

|---|---|

| Individual | $90,000 |

| Married couple | $180,000 |

This creates significant immediate estate reduction for families with multiple children or grandchildren.

Strategy 3: Advanced Trust Strategies for Substantial Wealth

For families whose estate exceeds what systematic gifting can address, trust structures separate legal ownership from beneficial enjoyment — removing assets from the estate while maintaining some connection to transferred wealth.

Grantor Retained Annuity Trusts (GRATs):

You transfer assets to a trust that pays you a fixed annuity for a specified term. If the assets appreciate beyond the annuity rate, that excess appreciation passes to beneficiaries without additional transfer taxes. GRATs work best for assets expected to appreciate significantly — business interests, growth investments, or concentrated stock positions.

Intentionally Defective Grantor Trusts (IDGTs):

You sell assets to a trust in exchange for a promissory note. You pay income taxes on the trust’s earnings (which reduces your estate), while the trust assets grow for beneficiaries without additional transfer tax consequences. The income tax payments function as additional tax-free gifts to the trust, compounding the benefit over time.

Both strategies require professional implementation. The concepts illustrate a key principle: sophisticated estate planning coordinates income and transfer tax systems simultaneously to create compounding benefits.

When to Start Planning in the Post-OBBBA Era

The OBBBA replaced artificial legislative deadlines with natural planning milestones. Think of estate planning as a lifecycle process, not a series of urgent responses to expiring laws.

| Life Stage | Age Range | Primary Planning Focus |

|---|---|---|

| Early career | 30s to 40s | Basic estate documents, understand your state’s rules, begin annual exclusion gifting if you have children |

| Mid-career | 40s to 50s | Systematic gifting programs, geographic planning if exposure is likely, consider advanced structures as wealth accelerates |

| Pre-retirement | 60s | Aggressive wealth transfer strategies while income is still high, model retirement withdrawal scenarios, coordinate with estate plan |

| Post-retirement | 70s+ | Dynamic withdrawal sequencing, legacy planning execution, coordinate Roth accounts and life insurance death benefits |

Natural planning milestones (post-OBBBA):

- Reaching your state’s estate tax threshold

- Significant asset appreciation events (real estate, business sale, stock options)

- Receiving an inheritance that increases your estate

- Major life changes — retirement, health concerns, family structure changes

Building Your Professional Team

Effective estate planning requires coordination across 4 types of professionals:

| Professional | Primary Role |

|---|---|

| Estate planning attorney | Legal structure design — trusts, wills, beneficiary coordination |

| Tax professional (CPA / EA) | Scenario modeling, gift tax compliance, income tax integration |

| Financial advisor | Integration with retirement and investment planning, liquidity analysis |

| Insurance specialist | Liquidity planning for estate taxes, wealth transfer enhancement through life insurance |

In the post-OBBBA environment, geographic planning makes professional coordination particularly important — residency changes involve legal, tax, and practical considerations that extend well beyond estate taxes.

What This Means for Different Types of Families

| Family Type | OBBBA Impact | Planning Priority |

|---|---|---|

| Middle-class, no-tax state | Estate taxes essentially eliminated | Focus on retirement funding, basic estate docs |

| Middle-class, high-tax state (OR, WA, MA) | Clearer decision framework — purely state optimization | Geographic planning, systematic gifting, or liquidity planning |

| High-net-worth (any state) | Certainty and higher exemptions enable longer-term horizons | Sophisticated trust strategies over extended timeframes without artificial deadlines |

The 3 Broader Lessons from the OBBBA

Uncertainty creates more planning pressure than actual tax burdens. Many families implemented expensive strategies to address federal exemption reductions that ultimately didn’t materialize. Planning against worst-case legislative outcomes has real costs.

Federal and state tax policies diverge — and that gap is now huge. The distance between a $30M federal exemption and Oregon’s $1M exemption has never been wider. Geographic planning has never been more valuable for families in high-tax states.

Permanent policy enables better planning than temporary provisions. Families can now implement strategies over natural timeframes — aligned with their life circumstances rather than artificial legislative deadlines.

This article is for educational and informational purposes only and should not be construed as legal, tax, or financial advice. Estate tax laws are complex and vary significantly by state and individual circumstances. The examples used throughout are hypothetical and for illustrative purposes only. Before implementing any estate planning strategies, consult with qualified professionals — including estate planning attorneys, tax advisors, and financial planners — who can provide advice tailored to your specific situation.