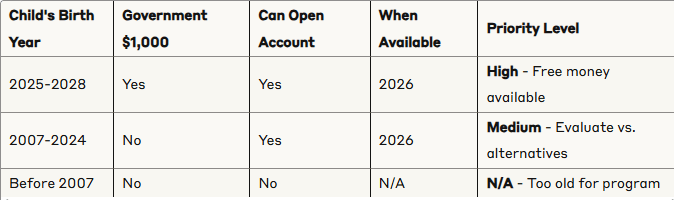

In July 2025, President Trump signed the “One Big Beautiful Bill” into law, creating new investment accounts for children under 18, with the government providing $1,000 in seed money for U.S. citizens born between 2025 and 2028. While these accounts have been nicknamed “Trump accounts” by Republican lawmakers, they represent something more significant than their political branding suggests.

Important timing note: Although the law was signed in July 2025, Trump accounts are expected to become available for opening starting in 2026. This gives financial institutions time to set up the required infrastructure and allows the IRS to issue detailed implementation guidance.

What Are Trump Accounts?

Think of Trump accounts as a hybrid between a traditional IRA and a college savings plan — with some unique characteristics that set them apart from both. At their core, they are tax-deferred retirement accounts specifically designed for American children, structured to be more accessible than traditional retirement accounts.

The fundamental concept: give every American child a financial stake in the country’s economic success from birth, allowing them to benefit from compound growth over nearly 2 decades before they enter the workforce.

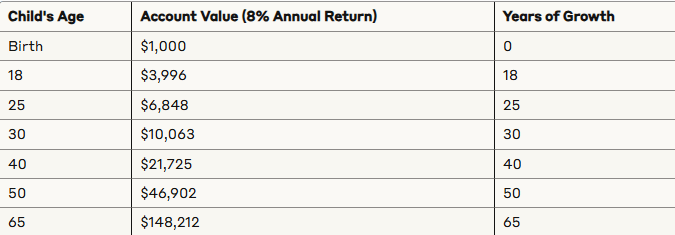

The $1,000 Head Start: How Powerful Is It?

Children born between January 1, 2025, and December 31, 2028, automatically qualify for a $1,000 deposit from the U.S. Treasury. The real power is in the compounding:

Time is the most powerful variable. Even with no additional contributions, that $1,000 provides a meaningful financial foundation — completely free.

Now consider what happens when parents maximize contributions. Contributing the full $5,000 annually for 18 years ($90,000 in contributions plus the government’s $1,000):

Consistent contributions over time compound dramatically — which is why these accounts have attracted so much attention.

How Contributions Work

| Feature | Details |

|---|---|

| Annual contribution limit | $5,000 per child (inflation-adjusted starting 2027) |

| Earned income requirement | None — unlike traditional or Roth IRAs |

| Employer contributions | Up to $2,500/year per employee’s child, tax-free to both employer and employee |

| Who can contribute | Parents, grandparents, employers, or any third party |

The earned income exemption removes a major barrier — parents can start retirement savings for very young children without waiting for the child to have a job.

The Employer Contribution Opportunity

Example — The Johnson Family:

- Sarah works for a tech company that offers Trump account contributions as a benefit

- Her employer contributes $2,500 per child annually (2 children)

- Sarah adds $2,500 per child from her own funds to reach the $5,000 maximum

- Total annual family contribution across both children: $10,000

- Sarah’s tax benefit: She avoids paying income tax on the $5,000 in employer contributions

We may start seeing Trump account contributions offered alongside health insurance and 401(k) matches as part of competitive employee benefit packages.

Example — Small Business Owner Strategy:

| Item | Details |

|---|---|

| Employees | 10, averaging 1.5 eligible children each |

| Employer contribution per child | $2,000 (below $2,500 max) |

| Total annual business cost | $30,000 (15 children x $2,000) |

| Business tax deduction | $30,000 |

| Employee value per family | $2,000 to $4,000 in tax-free benefits annually |

Investment Rules: Simplicity by Design

Trump account funds must be invested in low-cost index funds tracking major U.S. stock indexes (S&P 500 and similar). This constraint serves 3 purposes:

- Prevents poor investment choices that could devastate children’s accounts

- Guarantees low fees, which have an outsized impact on long-term returns

- Ties every participating child’s financial future to the success of American businesses

After the child turns 18, investment restrictions may be relaxed to allow the same range of options available in traditional IRAs.

Access Rules: When and How the Money Can Be Used

The money is completely inaccessible until the child reaches 18. Once the child turns 18, the account follows traditional IRA withdrawal rules — including the pro-rata rule.

Understanding the Pro-Rata Rule

Each withdrawal contains a mix of contributions (tax-free) and earnings (taxable).

Example — Sarah’s Trump Account at Age 22:

| Item | Amount |

|---|---|

| Total account value | $50,000 |

| Original contributions (incl. government seed) | $35,000 (70%) |

| Earnings | $15,000 (30%) |

On a $10,000 withdrawal:

- Tax-free portion (contributions): $7,000

- Taxable portion (earnings): $3,000

- Potential 10% early withdrawal penalty: $300

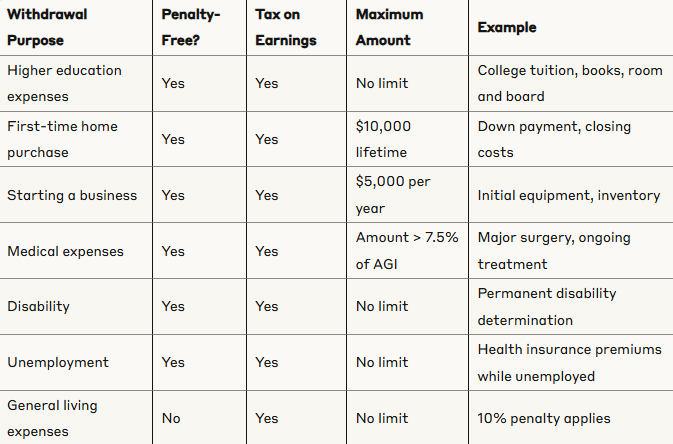

Penalty-Free Withdrawal Exceptions

3 scenarios that show how withdrawal rules play out:

Scenario 1 — College Student (Alex, age 20)

Account value: $45,000 ($30,000 contributions / $15,000 earnings). Needs $15,000 for junior year.

| Item | Amount |

|---|---|

| Tax-free portion (66.7% contributions) | $10,000 |

| Taxable earnings (33.3% earnings) | $5,000 |

| Penalty | $0 (education exception) |

| Income tax on earnings (12% bracket) | $600 |

| Net proceeds | $14,400 |

Scenario 2 — First-Time Homebuyer (Jessica, age 25)

Account value: $62,000 ($42,000 contributions / $20,000 earnings). Needs $8,000 for down payment.

| Item | Amount |

|---|---|

| Tax-free portion (67.7% contributions) | $5,419 |

| Taxable earnings (32.3% earnings) | $2,581 |

| Penalty | $0 (first-home exception) |

| Income tax on earnings (22% bracket) | $568 |

| Net proceeds | $7,432 |

Scenario 3 — Emergency Withdrawal, No Exception (Michael, age 24)

Account value: $55,000 ($38,000 contributions / $17,000 earnings). Needs $12,000.

| Item | Amount |

|---|---|

| Tax-free portion (69.1% contributions) | $8,291 |

| Taxable earnings (30.9% earnings) | $3,709 |

| Penalty (10% of earnings portion) | $371 |

| Income tax on earnings (22% bracket) | $816 |

| Net proceeds | $10,813 |

The True Cost of Early Withdrawals

A $20,000 withdrawal at age 25 ultimately costs over $300,000 in retirement wealth. This is why financial advisors consistently emphasize leaving retirement accounts untouched whenever possible.

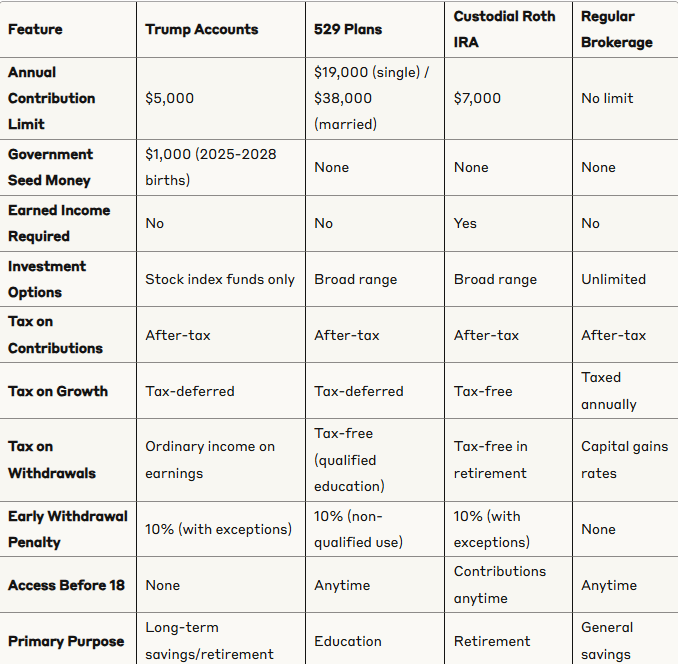

How Trump Accounts Compare to Other Savings Options

Trump Accounts vs. 529 College Savings Plans

529 plans remain the gold standard for college savings. The tax treatment difference is significant.

Scenario — The Martinez Family ($5,000/year, 18 years, 7% growth):

Both accounts reach approximately $180,000. But when Sofia starts college:

| Account | Taxes on Withdrawal | Net Available for College |

|---|---|---|

| 529 Plan | $0 (qualified education withdrawals are tax-free) | $180,000 |

| Trump Account | ~$19,800 (22% bracket on earnings portion) | $160,200 |

529 advantage: ~$20,000 more in usable funds for education.

529 plans also have no annual contribution cap ($5,000 limit constrains the Trump account significantly for high savers).

When Trump accounts win over 529s:

- Sofia receives scholarships covering most costs

- She chooses a trade school rather than a 4-year college

- Flexibility matters more than maximum tax efficiency for education

- The family wants a parallel wealth-building track beyond college

Trump Accounts vs. Custodial Roth IRAs

The critical difference: Roth IRAs require the child to have earned income. Trump accounts do not.

The Chen Family — Kevin (16, earns $3,000/year) vs. Emma (5, no income):

| Child | Custodial Roth IRA | Trump Account |

|---|---|---|

| Kevin (earned income) | Up to $3,000/year | Up to $5,000/year |

| Emma (no income) | $0 — cannot contribute | Up to $5,000/year + $1,000 government seed |

Long-term tax comparison for Kevin (identical $3,000/year contributions for 3 years, then left to grow):

The Roth IRA’s completely tax-free retirement withdrawals create a substantial long-term advantage. The Trump account’s ordinary income tax treatment at withdrawal is less favorable. For children with earned income, the Roth IRA is typically the superior retirement savings vehicle.

Trump Accounts vs. Regular Brokerage Accounts

The Williams Family ($5,000/year, 18 years):

| Feature | Regular Brokerage | Trump Account |

|---|---|---|

| Investment flexibility | Full (stocks, bonds, REITs, international) | Index funds only |

| Tax treatment | Annual taxes on dividends and capital gains | No annual taxes; ordinary income on withdrawal |

| Access | Anytime, any purpose | Locked until 18, then IRA-style rules |

| Government boost | None | $1,000 (if eligible) |

The Trump account’s tax-deferred growth provides a meaningful edge over 18 years — and that’s before counting the $1,000 government contribution. The brokerage account wins on one dimension only: immediate access before age 18.

Potential Drawbacks

Limited tax advantages: Tax-deferred growth is helpful, but ordinary income tax treatment on withdrawals is less favorable than Roth accounts (tax-free) or brokerage accounts (capital gains rates).

100% equity exposure throughout childhood: The index fund requirement prevents age-based rebalancing. Most financial advisors recommend shifting toward more conservative allocations as children approach college age — Trump accounts don’t allow this.

Complexity: The interaction between contribution limits, the pro-rata rule, and withdrawal exceptions is genuinely complicated and may deter some families.

Implementation uncertainty: Many important details about how accounts will work in practice remain subject to future IRS guidance. Rules may differ from what is described here.

5 Family Scenarios

Scenario 1: Young Professional Family (Starting to Save)

The Thompson Family: Jake earns $85,000, Maria earns $52,000. 2-year-old daughter Lily. Can save $200/month ($2,400/year).

| Strategy Component | Details |

|---|---|

| Annual Trump account contribution | $2,400 |

| Government seed money | $1,000 |

| Total 16-year contributions | $39,400 |

| Projected value at Lily’s age 18 (7% return) | $69,442 |

| If left untouched until retirement | $2,576,340 |

Why it works: The account’s flexibility allows Lily to use the money for education, a home down payment, or long-term wealth building — without forcing a choice upfront.

Scenario 2: High-Earning Family (Multiple Account Strategy)

The Rodriguez Family: Carlos (cardiologist, $350,000) and Linda (financial advisor, $125,000). 3 children ages 6, 9, and 12.

| Account Type | Annual per Child | Purpose |

|---|---|---|

| 529 Plans | $15,000 | College funding (superior tax treatment for education) |

| Trump Accounts | $5,000 | Retirement jumpstart — parallel track to 529 |

| Custodial Roth IRAs | Based on earned income | For summer job income when available |

| Total per child | $20,000+ |

Why it works: The family has already maxed college savings through 529s. Trump accounts serve as a parallel retirement wealth-building track that also captures any scenario where 529 funds go unused (scholarships, trade school, etc.).

Scenario 3: Business Owner (Employee Benefit Strategy)

Sarah’s Marketing Agency: 25 employees, seeking competitive benefits without dramatic cost increases.

| Component | Details |

|---|---|

| Employer contribution per child | $2,000 |

| Average children per employee | 1.2 (30 total contributions) |

| Annual business cost | $60,000 |

| Business tax deduction | $60,000 |

| Net cost after 25% tax rate | $45,000 |

| Value to employee with 2 children | $4,000/year tax-free; $64,000 over 16 years growing to ~$140,000 by age 18 |

Sarah’s personal strategy: She adds the employer contribution ($2,000/child) plus personal contributions ($3,000/child) to reach the $5,000 maximum for her own children.

Scenario 4: Grandparent Strategy

Robert and Helen: Retired, 8 grandchildren (newborn to age 16). Goal: visible legacy without complex trust structures.

- $5,000/year per grandchild

- Total annual gifting: $40,000

- Stays well below $18,000 annual gift tax exclusion per recipient

Robert and Helen can watch their grandchildren’s accounts grow during their lifetime while creating substantial wealth transfer — no gift tax returns required.

Scenario 5: Single Parent Strategy

Maria: Nurse, $68,000 income, 2 children (ages 7 and 10). Contributes $100/month when possible, misses some months.

| Child | Gov. Seed | Maria’s Contributions | Total | Projected at Age 18 |

|---|---|---|---|---|

| Child 1 (age 7) | $1,000 | $9,600 (8 of 11 years) | $10,600 | $23,891 |

| Child 2 (age 10) | $1,000 | $7,200 (6 of 8 years) | $8,200 | $16,847 |

Even modest, inconsistent contributions build meaningful financial foundations. If either child leaves their account untouched until retirement, those figures compound into substantially larger sums.

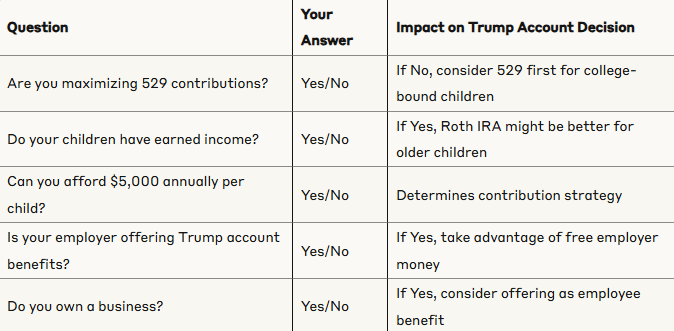

Practical Next Steps

Step 1: Determine Eligibility and Plan for 2026

Key point: Accounts are not available yet. Use the remainder of 2025 to research providers and plan your contribution strategy.

Step 2: Assess Your Current Savings Strategy

Step 3: Choose Your Contribution Strategy

| Strategy | Annual Contribution | Best For | Projected Value at Age 18 |

|---|---|---|---|

| Conservative | $1,000 to $2,000 | Families just starting out | $50,000 to $100,000 |

| Balanced | $4,000 to $5,000 (incl. employer) | Middle-income families | $150,000 to $200,000 |

| Aggressive | $5,000 max + coordination | High-earning families | $200,000+ |

Implementation Timeline

| Year | Actions |

|---|---|

| 2025 | Research providers; calculate contribution amounts; coordinate with financial advisor; design employer benefit structure if applicable; monitor IRS guidance |

| 2026 | Open accounts as soon as institutions offer them; set up automatic contributions; claim $1,000 government seed for eligible children; launch employer programs if applicable |

| 2027 to 2043 | Make consistent annual contributions; claim seed money for 2027 to 2028 births; review strategy as children approach 18 |

| Post-2043 | Help adult children understand withdrawal options; coordinate with college financing; consider conversion strategies |

Recommended Savings Priority Order

- Family emergency fund

- Employer 401(k) match

- High-interest debt elimination

- 529 contributions (if college is the primary goal)

- Trump account contributions

- Additional retirement savings

4 Common Mistakes to Avoid

Mistake 1: Waiting to start. Every month of delay is compound growth lost. Earlier contributions in the same year outperform later ones by hundreds of dollars per child.

Mistake 2: Focusing only on the $1,000 government money. The free seed is a starting point, not the strategy.

| Scenario | Value at Age 18 |

|---|---|

| Government $1,000 only | ~$4,000 |

| Government $1,000 + $2,000/year | ~$81,000 |

Additional contributions create roughly 20 times more value than the seed money alone.

Mistake 3: Not coordinating with other savings goals. Trump accounts are a complement to 529s and Roth IRAs, not a replacement.

Mistake 4: Choosing the wrong financial institution. Since all Trump accounts must hold index funds, fees are the only differentiator. Compare: annual account fees, expense ratios of available index funds, platform usability, and customer service quality.

The Broader Picture

Economic experts have long advocated for “baby bonds” as a way to introduce more Americans to investing and address wealth inequality. Trump accounts are the first large-scale implementation of this concept in American policy, at a projected cost of approximately $17 billion over 10 years.

Some economists argue that a more progressive version — with larger initial contributions for lower-income families — would more effectively address wealth inequality. However, the universal nature of Trump accounts ensures broad political support.

What’s certain: any program that introduces children to compound growth from birth deserves serious consideration, especially when it includes a $1,000 head start. Accounts become available in 2026. Start planning now.

This article is for educational and informational purposes only and should not be construed as personalized financial, investment, tax, or legal advice. The information is based on current understanding of the One Big Beautiful Bill as of August 2025, but implementation details, rules, and regulations may change as federal agencies issue additional guidance. Trump accounts are expected to become available in 2026 — exact timing and participating financial institutions have not yet been finalized. All projections and examples are hypothetical and for illustrative purposes only. Consult qualified financial advisors, tax professionals, and estate planning attorneys before making any financial decisions.