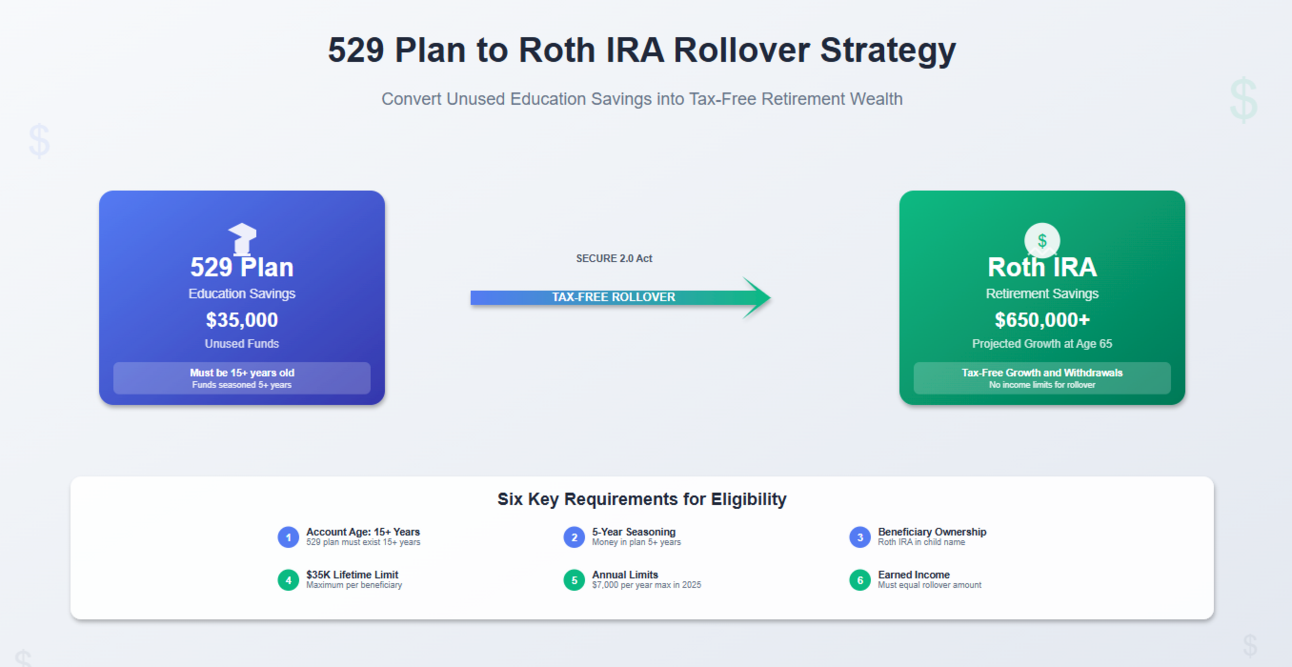

Spending 18 years carefully building a college fund, only to discover your child earned a full scholarship, chose a trade career, or needed less than you saved — that used to mean a painful choice: pay steep penalties to access the money, leave it sitting unused, or redirect it to family members who might not need it.

The SECURE 2.0 Act changed this in late 2022. For the first time, families can redirect substantial unused 529 funds directly into Roth retirement accounts without triggering the taxes and penalties that normally apply. A seemingly modest $35,000 transfer can grow into over $560,000 in tax-free retirement wealth. But accessing this opportunity requires navigating 6 specific requirements that most families — and many advisors — don’t fully understand.

The 6 Eligibility Requirements

These are not arbitrary hurdles. Each reflects a specific tax policy goal. Understanding the reasoning behind each rule helps you plan more effectively.

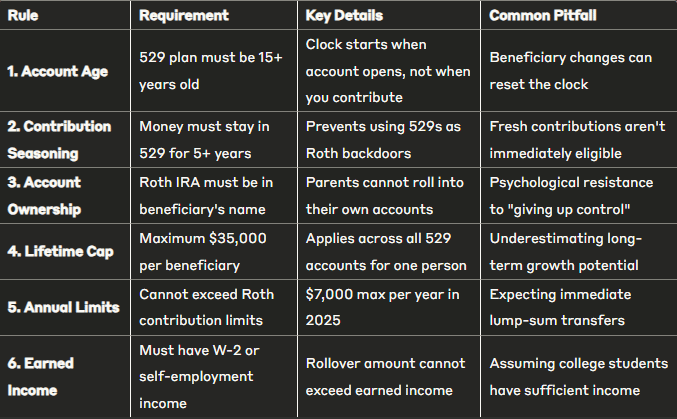

Requirement 1: Account Maturity — The 15-Year Rule

The 529 account must have existed for at least 15 years before any rollover is eligible. The clock starts from the account opening date — not from when contributions were made, and not from when the account reached a certain balance.

Critical nuance: Changing the beneficiary on an existing account often resets the 15-year clock. This is one of the most common planning mistakes families make. Parents who move funds between siblings by changing beneficiaries may unknowingly destroy rollover eligibility that took years to develop.

Planning implication: Open separate accounts for each child rather than relying on beneficiary changes to redirect funds. Each account maintains its own independent 15-year timeline.

Requirement 2: Contribution Seasoning — The 5-Year Waiting Period

Contributions must sit in the 529 for at least 5 years before becoming rollover-eligible. This prevents families from contributing fresh money and immediately redirecting it to Roth accounts — which would effectively allow unlimited Roth conversions through the 529 wrapper.

Contributions made today won’t be rollover-eligible for 5 years. Families who contribute consistently over many years will have multiple “vintage years” reaching eligibility at different points, providing ongoing flexibility for timing transfers.

Requirement 3: Account Ownership — The Roth IRA Must Be in Your Child’s Name

The Roth IRA receiving rollover funds must be in the beneficiary’s name — your child’s — not yours. You cannot redirect unused education savings into your own retirement accounts.

This restriction is actually a wealth-building opportunity in disguise. Most young adults receive no meaningful retirement account funding until well into their careers. This rule mandates that you are providing early-career retirement savings for your child at the exact age when compound growth has its greatest long-term impact.

Requirement 4: Lifetime Limit — $35,000 per Beneficiary

The maximum lifetime rollover is $35,000 per beneficiary, regardless of how many 529 accounts they are associated with or how much sits in those accounts.

This limit applies across their entire lifetime — it is not an annual figure, and it cannot be reset.

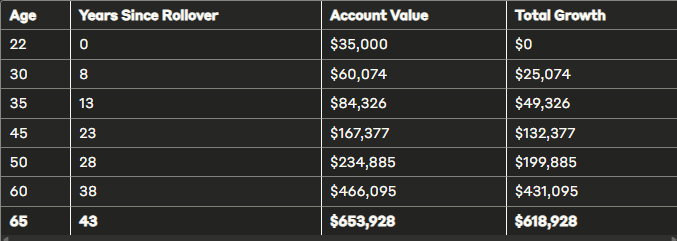

Why $35,000 matters more than it looks:

| Age at Rollover | Years to Age 67 | Value at 67 (7% return) |

|---|---|---|

| 22 | 45 | $560,000+ |

| 25 | 42 | $463,000+ |

| 30 | 37 | $329,000+ |

All growth is completely tax-free. These projections assume no additional contributions beyond the initial $35,000 rollover. The earlier the transfer occurs, the more dramatically compound growth amplifies the outcome.

Requirement 5: Annual Pacing — Capped at Roth IRA Contribution Limits

You cannot roll the full $35,000 in a single year. Annual rollover amounts are capped at the current Roth IRA contribution limit ($7,000 for individuals under 50 as of the current IRS guidelines). At that rate, hitting the $35,000 lifetime maximum takes a minimum of 5 years.

This pacing requirement forces sustained coordination between the 529 account and your child’s career and income timeline — which leads directly to the most restrictive requirement.

Requirement 6: Earned Income — Equal to or Greater Than the Rollover Amount

For each year a rollover is executed, the beneficiary must have earned income equal to or greater than the amount being rolled over. Investment income, gifts, and passive income do not qualify.

| Child’s Earned Income | Maximum Rollover That Year |

|---|---|

| $0 (graduate student, unpaid intern) | $0 |

| $4,000 (part-time work) | $4,000 |

| $7,000+ | $7,000 (the annual cap) |

No earned income means no rollover eligibility — regardless of how much sits in the 529 or how old the account is.

Key planning implication: Summer jobs, part-time employment, freelancing, and entrepreneurial work during high school and college are not just income — they are future rollover eligibility. Every dollar of earned income creates a dollar of rollover capacity.

The Income Limit Bypass — A Significant Hidden Benefit

Under normal circumstances, high earners face Roth IRA contribution phase-outs based on adjusted gross income. Single filers above certain income thresholds are eventually prohibited from making direct Roth contributions entirely.

529-to-Roth rollovers are completely exempt from these income limits.

A young professional earning well above the normal Roth phase-out threshold is still eligible for 529 rollovers as long as they meet the 6 requirements above. For families investing heavily in their children’s education and career development, this creates a valuable Roth access pathway that would otherwise be unavailable to high earners.

Tax Treatment: Federal and State

Federal: Completely Tax-Free

529-to-Roth rollovers under SECURE 2.0 are treated as qualified rollovers between tax-advantaged accounts. No federal income taxes. No 10% early withdrawal penalty. The full transfer amount moves intact.

This contrasts sharply with non-qualified 529 withdrawals, which trigger both ordinary income tax and a 10% penalty on earnings.

State Tax Treatment: Varies Significantly

| State Category | States | Tax Treatment |

|---|---|---|

| Follows federal — no recapture | Alabama, Arizona, Delaware, Georgia, Hawaii, Idaho, Kansas, Kentucky, Maine, Maryland, Nebraska, New Mexico, North Carolina, North Dakota, Ohio, Oregon, Pennsylvania, South Carolina, Virginia, West Virginia, Wisconsin | Rollovers are tax-free; no recapture of prior state deductions |

| Requires recapture of prior deductions | Illinois, Indiana, Iowa, Massachusetts, Michigan, Minnesota, Montana, New York, Utah, Vermont | Prior state deductions for 529 contributions must be added back to state taxable income |

| No state income tax | Alaska, Florida, Nevada, New Hampshire, South Dakota, Tennessee, Texas, Washington, Wyoming | State tax irrelevant |

| California — additional state tax | California | Treats rollovers as non-qualified withdrawals AND imposes an additional 2.5% state tax on the earnings portion |

| Pending or unclear | Arkansas, Colorado, Connecticut, Louisiana, Mississippi, Missouri, New Jersey, Oklahoma, Rhode Island, DC | Position not yet announced; consult a local tax professional |

Virginia example: Residents can claim up to $4,000 in annual state tax deductions for 529 contributions and still execute rollovers without recapture. No repayment of the original state tax benefit required.

California example: The 2.5% additional state tax makes California the least favorable state for this strategy, though federal benefits may still justify execution depending on the account balance and the individual’s tax situation.

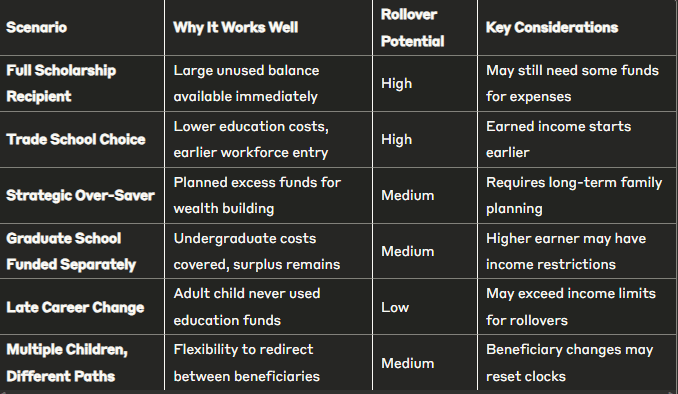

Who Benefits Most: 4 Family Scenarios

Scenario 1: The Scholarship Family

A family saved $150,000 for a child’s education. Scholarship awards cover $100,000 of actual costs. The remaining $50,000 represents successful planning that exceeded expectations — not a waste.

Through rollover planning, up to $35,000 of those excess funds can begin generating tax-free retirement wealth. The remainder can be redirected to other family members, held for graduate school, or withdrawn subject to standard penalty rules.

Scenario 2: The Alternative Path

A child chooses a trade school, apprenticeship, or direct workforce entry instead of a traditional 4-year degree. Costs are far lower than anticipated, leaving substantial 529 balances available.

The narrative shifts: this is not money wasted on a plan that changed. It is education savings that funded career flexibility — and can now fund retirement security.

Scenario 3: The Prudent Over-Saver

Consistent contributions over many years, combined with strong investment returns, produce a 529 balance that exceeds reasonable education cost estimates. Rather than treating this as a planning error, it can be structured as the first stage of a multi-generational wealth building strategy.

Scenario 4: The High-Earning Child

A child who earns above the normal Roth IRA income phase-out thresholds gains access to Roth benefits through the rollover pathway that would otherwise be unavailable. The more professionally successful the child becomes, the more valuable this tax-free transfer becomes — because they face higher marginal rates and fewer alternative Roth access options.

Common Implementation Mistakes

Mistake 1: Miscounting the 15-year clock

Many families discover too late that a beneficiary change or account restructuring reset the timeline. Maintain documentation of the original account opening date and avoid unnecessary beneficiary modifications.

Mistake 2: Assuming earned income will always be available

Demanding academic programs, unpaid internships, and graduate school years can produce low or zero earned income years. A student with no earned income in a given year has zero rollover eligibility that year, regardless of how much sits in the 529. Plan for income gaps and front-load rollovers during high-income years.

Mistake 3: Forgetting to coordinate with direct Roth contributions

Rollover amounts count toward the annual Roth IRA contribution limit. If your child is already making Roth contributions from employment income, those reduce the rollover capacity for the same year. Track both sources together.

Mistake 4: Ignoring state tax recapture requirements

Families in recapture states who don’t account for state-level consequences may face unexpected state income tax bills. Model the state tax cost alongside the federal benefit before executing.

Mistake 5: Multi-state contribution history

Families who lived in multiple states during their savings years may face complex allocation questions. A family that claimed Virginia deductions for 10 years, then moved to Massachusetts for 5, needs to understand how to allocate rollovers across contributions made under different state tax regimes.

Implementation Strategy

Phase 1: Foundation Building (Birth Through High School)

| Action | Why It Matters |

|---|---|

| Open accounts early, ideally at or near birth | Starts the 15-year clock immediately |

| Open separate accounts per child | Avoids beneficiary changes that reset the clock |

| Contribute consistently, even small amounts | Creates multiple “vintage years” of 5-year-seasoned funds |

| Encourage part-time work and entrepreneurial activity | Builds earned income record for future rollover eligibility |

Phase 2: Active Rollover Period (Early Career)

| Action | Why It Matters |

|---|---|

| Verify 15-year account eligibility | Confirm clock was never reset by beneficiary changes |

| Confirm 5-year seasoning on specific contributions | Newer contributions are not yet eligible |

| Coordinate with child’s earned income each year | Rollover cannot exceed that year’s earned income |

| Track against annual Roth contribution limit | Direct Roth contributions reduce rollover capacity |

| Model state tax consequences | Especially critical in recapture states and California |

Phase 3: Coordination with Broader Financial Goals

Time rollovers to coincide with lower-income years when possible — lower income means the Roth conversion effectively occurs at a lower marginal rate. Coordinate with employer 401(k) matching opportunities, as maximizing matching contributions before pursuing rollovers typically produces better overall outcomes. Consider how rollovers interact with major life transitions such as home purchases, graduate school funding, and marriage.

Annual Rollover Pacing Example

Assuming a 22-year-old beneficiary with consistent earned income of $7,000+ per year:

| Year | Annual Rollover | Cumulative Total | Years Until $35K Lifetime Max |

|---|---|---|---|

| Year 1 | $7,000 | $7,000 | 5 years total |

| Year 2 | $7,000 | $14,000 | |

| Year 3 | $7,000 | $21,000 | |

| Year 4 | $7,000 | $28,000 | |

| Year 5 | $7,000 | $35,000 | Maximum reached |

At 7% annual growth, the Year 1 transfer alone grows to approximately $54,700 by the time the Year 5 transfer is made — before a single dollar of that final transfer has compounded at all.

Evaluating Whether This Strategy Fits Your Family

| Factor | Favors This Strategy | Works Against It |

|---|---|---|

| 529 account age | Account opened 15+ years ago | Account opened recently |

| Unused balance | Significant balance relative to remaining education costs | Funds still needed for education |

| Child’s career path | Earning income in early career | Graduate school, low-income years ahead |

| State of residence | No-recapture state or no income tax state | California or recapture state |

| Planning horizon | Comfortable with multi-year execution | Prefer simpler, immediate solutions |

| Asset control preference | Comfortable transferring assets to child’s name | Prefer maintaining centralized control |

| Organization and recordkeeping | Strong documentation systems | Difficulty maintaining long-term records |

The Broader Picture: Multi-Generational Wealth Implications

Roth IRAs have no required minimum distributions during the owner’s lifetime. Assets can continue growing tax-free indefinitely. Upon the owner’s death, the account transfers to beneficiaries who can receive distributions — potentially tax-free — over their own lifetimes.

A $35,000 rollover at age 22 is not just a retirement account contribution. It is the seed of a financial asset that, if left largely intact, can span multiple generations. Most young adults never receive meaningful retirement account funding until their 30s or 40s. A Roth IRA established in their early 20s through a 529 rollover gives them nearly two additional decades of compounding — a head start that cannot be replicated later regardless of how much they save.

Key Takeaways

| Rule | The Requirement |

|---|---|

| Account age | 529 must be at least 15 years old |

| Contribution seasoning | Money must be in the account for at least 5 years |

| Account ownership | Roth IRA must be in the beneficiary’s name |

| Lifetime cap | $35,000 per beneficiary, across all rollovers, ever |

| Annual pacing | Limited to the current Roth IRA contribution limit per year |

| Earned income | Beneficiary must have earned income equal to or greater than the rollover amount |

| Income limits | None — high earners qualify regardless of AGI |

| Tax treatment (federal) | Completely tax-free |

| Tax treatment (state) | Varies — research your specific state before executing |

This article is for educational and informational purposes only and should not be construed as personalized financial, tax, or legal advice. Tax laws are complex and subject to change. The SECURE 2.0 provisions discussed here may be modified by future legislation, and state tax treatment continues to evolve as states issue guidance. Consult a qualified tax professional, CPA, enrolled agent, or financial advisor who can evaluate your specific situation before implementing any strategy discussed in this article.